Laurus Labs reported its results yesterday

The company saw a 88% erosion in profits!😥😥😥

The recovery of the business is taking longer than expected

What is happening with Laurus Labs?🤔🤔

A thread🧵on the business performance of Laurus Labs

Lets go👇

The company saw a 88% erosion in profits!😥😥😥

The recovery of the business is taking longer than expected

What is happening with Laurus Labs?🤔🤔

A thread🧵on the business performance of Laurus Labs

Lets go👇

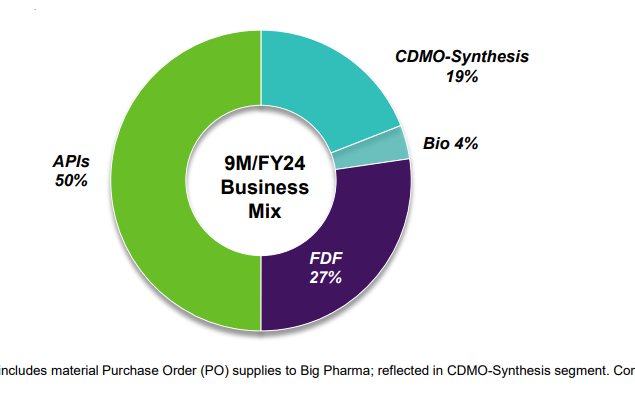

What does Laurus labs do?

Laurus Labs operates in the following areas:-

1. Active Pharmaceutical Ingredient(APIs)

2. Custom Synthesis

3. Formulations(FDF)

4. Biosynthesis

Laurus Labs operates in the following areas:-

1. Active Pharmaceutical Ingredient(APIs)

2. Custom Synthesis

3. Formulations(FDF)

4. Biosynthesis

Major focus in APIs is on ARV, oncology and other APIs. It owns 11 manufacturing units (six FDA approved sites) with 74 DMFs, 32 ANDAs filed (15 Para IV, 11 first to file) and 192 patents granted

China+1 playing out:-

Sourcing from China:-

Generic or big Pharma for custom synthesis+APIs is very difficult!

Big Pharma wants to reduce its dependency on China India will have a lot of opportunities in custom synthesis and APIs

Sourcing from China:-

Generic or big Pharma for custom synthesis+APIs is very difficult!

Big Pharma wants to reduce its dependency on China India will have a lot of opportunities in custom synthesis and APIs

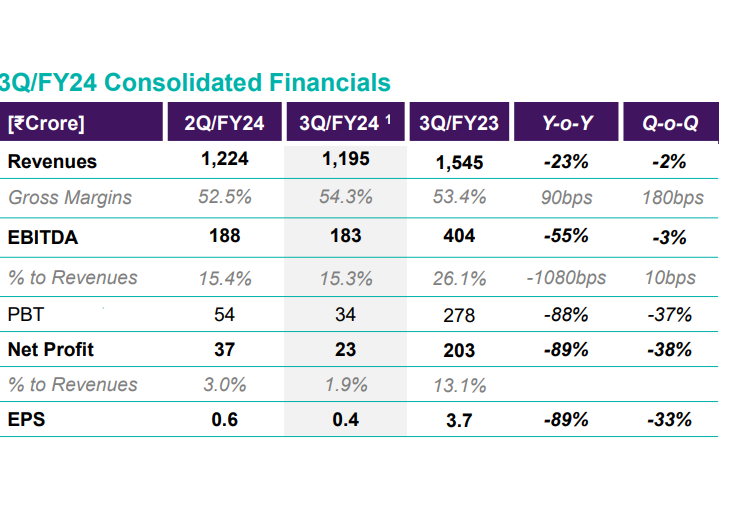

So how were the Q3FY24 results?

The results were not good

🧪Revenue declined by 23%

🧪Operating Margins eroded to just 15.3%

🧪Net profit fell by 88%

So what happened here?👇

The results were not good

🧪Revenue declined by 23%

🧪Operating Margins eroded to just 15.3%

🧪Net profit fell by 88%

So what happened here?👇

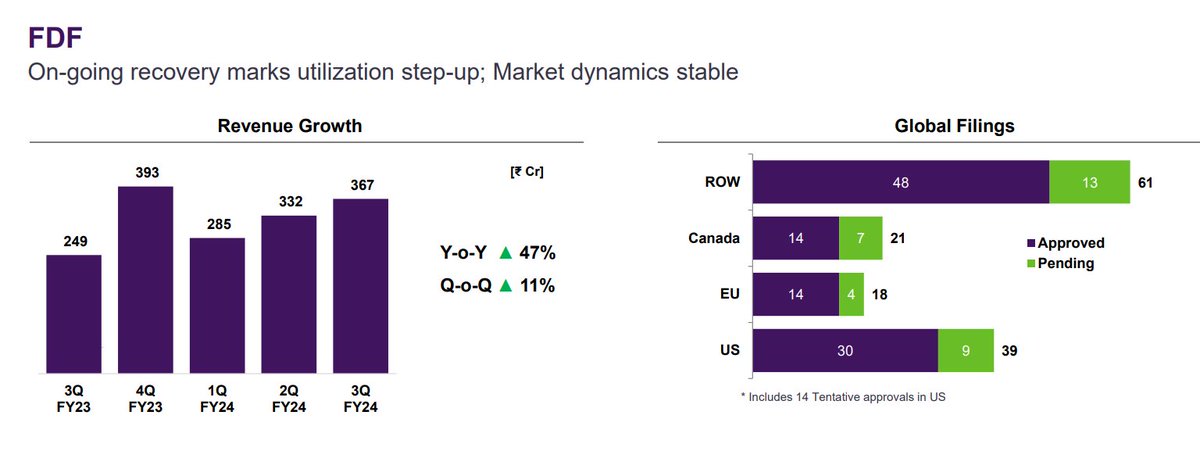

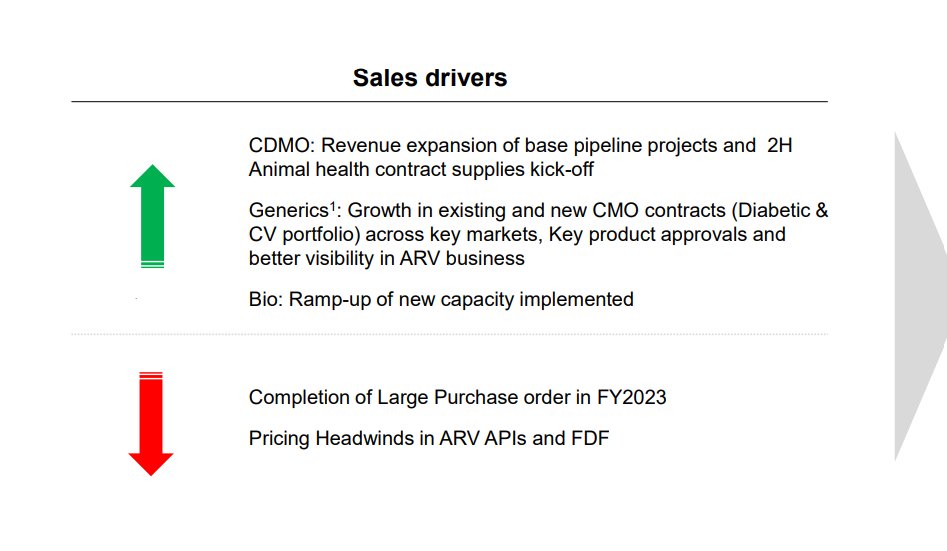

Fomulations business(FDF)-

FDF business saw a good sequential recovery of 11%

The underlying demand trend remains healthy with new tender wins.

The management expects continued recovery in this business driven by market share gains

FDF business saw a good sequential recovery of 11%

The underlying demand trend remains healthy with new tender wins.

The management expects continued recovery in this business driven by market share gains

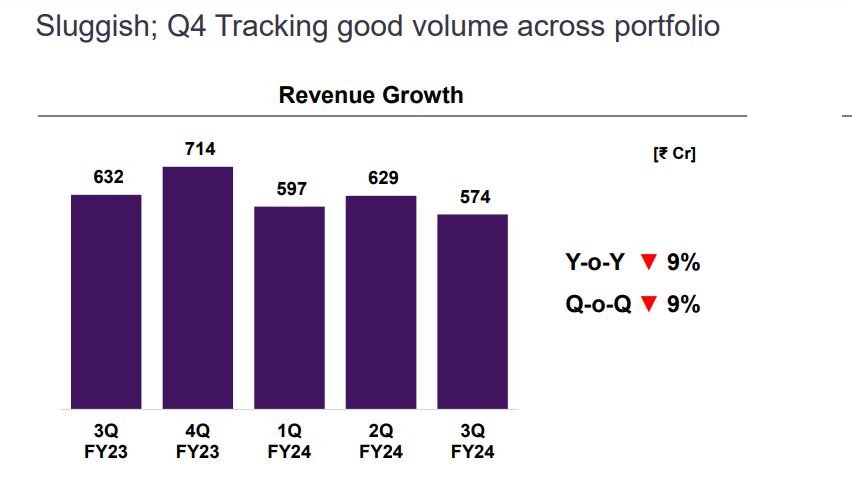

APIs:

API business saw a sluggish offtake.

It fell by 9% both yearly and quarterly.

Subdued pricing in API was seen.

The management expect better delivery in the Oncology and the ARV API from Q4

API business saw a sluggish offtake.

It fell by 9% both yearly and quarterly.

Subdued pricing in API was seen.

The management expect better delivery in the Oncology and the ARV API from Q4

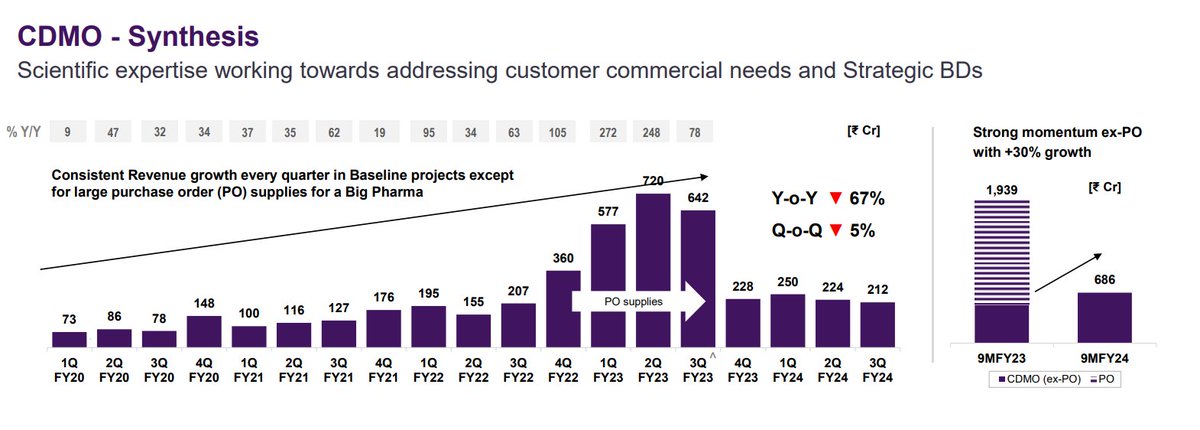

Custom Synthesis Business Leads:-

Custom Synthesis business saw a sharp decline owing to a higher base

Expansion in CDMO capabilities on track to capture new opportunities and accelerate growth

Custom Synthesis business saw a sharp decline owing to a higher base

Expansion in CDMO capabilities on track to capture new opportunities and accelerate growth

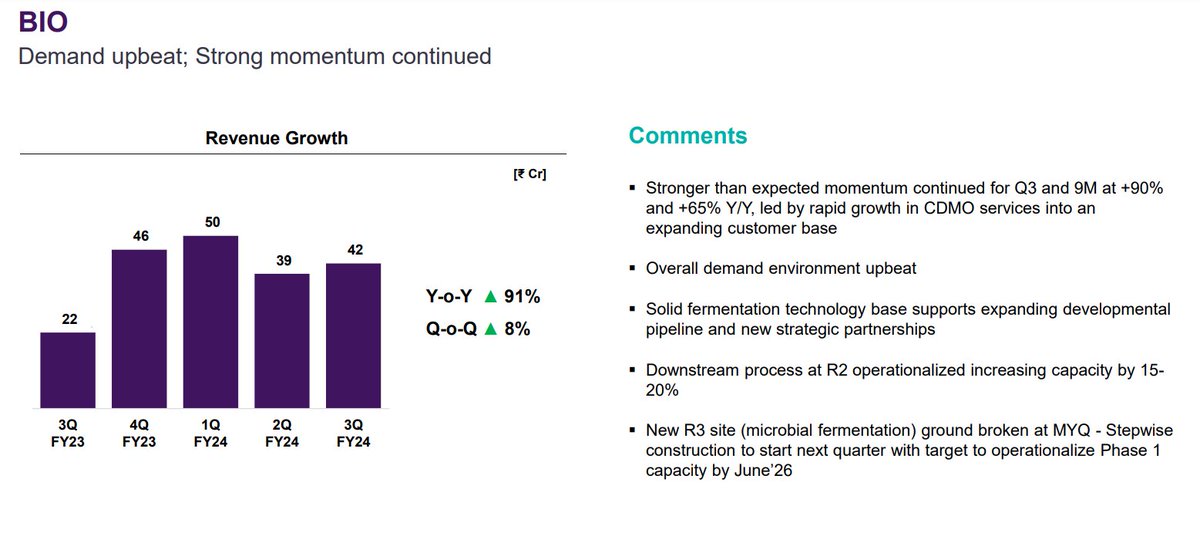

Laurus Bio:-

The business has a small base.

It will continue to ramp up slowly.

The ramp up has been now pushed back by at least an year

The business has a small base.

It will continue to ramp up slowly.

The ramp up has been now pushed back by at least an year

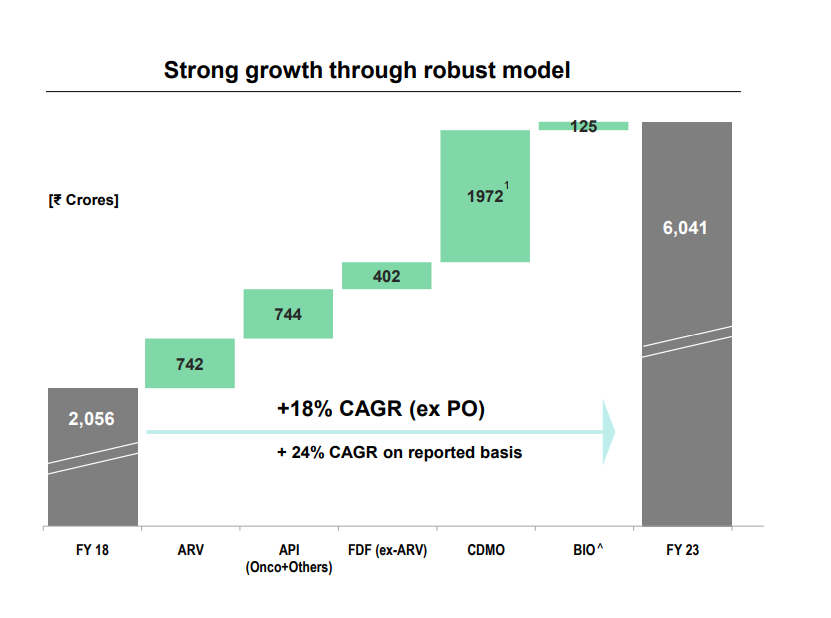

Laurus Labs was once just an ARV API player

Over the last 5 years they have brilliantly diversified into

1. Other APIs

2. CDMO

3. FDF

4. Laurus Bio

A story of strong execution

Over the last 5 years they have brilliantly diversified into

1. Other APIs

2. CDMO

3. FDF

4. Laurus Bio

A story of strong execution

Management Commentary

Management commentary:-

🧪Pricing headwinds in ARV API and FDF

🧪As guided FY24 will be a year of consolidation

🧪No revenue guidance for the year

🧪Margins have probably bottomed out

Management commentary:-

🧪Pricing headwinds in ARV API and FDF

🧪As guided FY24 will be a year of consolidation

🧪No revenue guidance for the year

🧪Margins have probably bottomed out

🧪In FY25 animal health CDMO will be a key trigger

🧪Large volume APIs will commercialize in FY25

🧪Laurus Bio will continue to see a ramp up

🧪Large volume APIs will commercialize in FY25

🧪Laurus Bio will continue to see a ramp up

Has the margin bottomed out?

🧪ARV and FDF offtake is recovering slower than expected

🧪Pricing pressure is already there

Margins have probably bottomed out

🧪ARV and FDF offtake is recovering slower than expected

🧪Pricing pressure is already there

Margins have probably bottomed out

Risks/monitorable to the business:

Most of Laurus's new facilities come online at end of FY24 and FY25:

🧪Any delay in commercialization can be a material risk to the business.

🧪Pricing pressure and slower demand in the API / FDF space remain concerns.

Most of Laurus's new facilities come online at end of FY24 and FY25:

🧪Any delay in commercialization can be a material risk to the business.

🧪Pricing pressure and slower demand in the API / FDF space remain concerns.

🧪Ramp up in CDMO and Biotechnology segments

🧪Delay in the procurement of APIs in the developed world

🧪Delay in the procurement of APIs in the developed world

Valuation:-

Given the strong pipeline of expansion in the coming two years

Laurus now trades at roughly 15x EV/EBITDA

The Valuation is certainly not cheap

Given the strong pipeline of expansion in the coming two years

Laurus now trades at roughly 15x EV/EBITDA

The Valuation is certainly not cheap

Conclusion:-

🧪Laurus's core API and FDF business have started to recover slower than expected

🧪Despite management guidance of pricing erosion bottoming out. There was further price erosion

🧪While the management remains optimistic,the ramp-up remains to be seen

🧪Laurus's core API and FDF business have started to recover slower than expected

🧪Despite management guidance of pricing erosion bottoming out. There was further price erosion

🧪While the management remains optimistic,the ramp-up remains to be seen

🧪CDMO business should start to to do well from Q3

🧪Laurus Bio should also start to do well

🧪Laurus Bio should also start to do well

Laurus labs is a story of a company diversifying its API base with brilliant execution over the last 5 years.

The API and FDF businesses are undergoing a downcycle.

But what goes into a upcycle will definitely bottom out and go into an upcycle

The API and FDF businesses are undergoing a downcycle.

But what goes into a upcycle will definitely bottom out and go into an upcycle

When will the cycle bottom out and move up?

According to the management, the business has bottomed out now and should start to improve from H2 onwards.

However, this needs to be closely monitored

According to the management, the business has bottomed out now and should start to improve from H2 onwards.

However, this needs to be closely monitored

Keep following me -@AdityaD_Shah as I write daily to make you aware around:

📈Personal Finance

📈Investing

📈Stock Analysis

Go to my profile and hit the bell icon🔔to always stay updated

📈Personal Finance

📈Investing

📈Stock Analysis

Go to my profile and hit the bell icon🔔to always stay updated

Disclaimer:-

This is my own study

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

This is my own study

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

Loading suggestions...