🏦India Shelter Finance Corporation Ltd: Offering Home Loans and Loans against Property for low and middle-income groups.

Detailed Company Analysis🧵👇

Detailed Company Analysis🧵👇

✍️Company Overview:

🔸India Shelter Finance Corporation Ltd was originally incorporated as "Satyaprakash Housing Finance India Limited" on October 26, 1988. In 2009, Mr. Anil Mehta gained control of the company, leading to a name change to "India Shelter Finance Corporation Ltd."

🔸India Shelter Finance Corporation Ltd was originally incorporated as "Satyaprakash Housing Finance India Limited" on October 26, 1988. In 2009, Mr. Anil Mehta gained control of the company, leading to a name change to "India Shelter Finance Corporation Ltd."

🔸Company primarily focuses on affordable housing finance for retail customers and operates 203 branches primarily in Rajasthan, Maharashtra, Madhya Pradesh, and Karnataka covering 94% of the Indian housing finance market.

🔸It has a robust technology infrastructure and focus on self-employed customers, especially first-time homebuyers in Tier II and Tier III cities.

✍️Business Vertical:

⚡️Co offers Home Loans and Loans against Property to low and middle-income segments in India, using technology and analytics, with interest rates between 10.5% to 20% per An and average loan sizes of 0.5 Mn to 5 Mn rupees.

⚡️Co offers Home Loans and Loans against Property to low and middle-income segments in India, using technology and analytics, with interest rates between 10.5% to 20% per An and average loan sizes of 0.5 Mn to 5 Mn rupees.

🔸Home Loans: Co provides home loans for various purposes like repairs, upgrades, self-construction, plot purchase, and property acquisition.

🔸Loan Against Property: Co offers secured loans using self-occupied residential properties as collateral.

🔸Loan Against Property: Co offers secured loans using self-occupied residential properties as collateral.

✍️Geographical AUM Bifurcation:

🔸Tier 1: 10.5% in FY23 vs 10% in FY22

🔸Tier 2: 42.5% in FY23 vs 45% in FY22

🔸Tier 3: 47% in FY23 vs 45% in FY22

🔸Tier 1: 10.5% in FY23 vs 10% in FY22

🔸Tier 2: 42.5% in FY23 vs 45% in FY22

🔸Tier 3: 47% in FY23 vs 45% in FY22

✍️Key Metrics:

🔸M Cap: ₹6,787 Cr

🔸P/E: 43.8

🔸CMP: ₹634

🔸ROE: 13.4%

🔸Assets Under Management: ₹ 5,181 Cr

🔸Net Interest Margin: 10.6%

🔸Net NPA Ratio: 0.72%

🔸Return on Assets: 4.12%

🔸Capital Risk Adequacy Ratio: 48.7

🔸Provision Coverage Ratio: 28.74%

🔸M Cap: ₹6,787 Cr

🔸P/E: 43.8

🔸CMP: ₹634

🔸ROE: 13.4%

🔸Assets Under Management: ₹ 5,181 Cr

🔸Net Interest Margin: 10.6%

🔸Net NPA Ratio: 0.72%

🔸Return on Assets: 4.12%

🔸Capital Risk Adequacy Ratio: 48.7

🔸Provision Coverage Ratio: 28.74%

✍️Financials Highlights:

🔸Revenue in FY23 at ₹584 Cr⬆️36% YOY.

🔸In FY23, Net interest income ⬆️to ₹293 Cr with a 32% CAGR from FY21-23.

🔸Net profit ⬆️from ₹87 Cr to ₹155 Cr, showing a 33% CAGR from FY21-23.

🔸TTM EPS at ₹35.32

🔸Revenue in FY23 at ₹584 Cr⬆️36% YOY.

🔸In FY23, Net interest income ⬆️to ₹293 Cr with a 32% CAGR from FY21-23.

🔸Net profit ⬆️from ₹87 Cr to ₹155 Cr, showing a 33% CAGR from FY21-23.

🔸TTM EPS at ₹35.32

✍️Key Highlights:

🔸Co serves low to middle-income customers, with 70.7% first-time home loan applicants in Tier II and Tier III Indian cities.

🔸Over the past 2.5 years, the asset quality of the company have improved.

🔸Co serves low to middle-income customers, with 70.7% first-time home loan applicants in Tier II and Tier III Indian cities.

🔸Over the past 2.5 years, the asset quality of the company have improved.

🔸Co maintains a strong asset quality with GNPA at 1.00%, NNPA at 0.72%, and 68.9% of customers with a credit score of 650+ as of September 2023.

🔸Co achieved a strong two-year CAGR of 40.8% in Assets Under Management (AUM).

🔸Co achieved a strong two-year CAGR of 40.8% in Assets Under Management (AUM).

🔸The average Loans Against Property ticket size in FY23 was ₹10 lakhs, with an average tenure of 11 years.

🔸The average ticket size of these loans in FY23 was ₹11 lakhs with average tenure of 15 years.

🔸During H1 FY24, 98.5% of disbursed loans were originated in-house.

🔸The average ticket size of these loans in FY23 was ₹11 lakhs with average tenure of 15 years.

🔸During H1 FY24, 98.5% of disbursed loans were originated in-house.

🔸Co has been able to maintain an average sanction loan-to-value (LTV) on portfolio low at 50.9% with 55.1% for home loans and 45.3% for LAP.

🔸As of September 30, 2023, 70.6% of AUM from self-employed customers, and 70.7% are first-time home loan takers.

🔸As of September 30, 2023, 70.6% of AUM from self-employed customers, and 70.7% are first-time home loan takers.

✍️IPO details:

🔸Co recently issued 24,340,771 Equity Shares through an IPO priced at ₹469 to ₹493 per share on December 13, 2023.

🔸The objective of issuing an IPO is to raise funds for future capital requirements towards onward lending and General corporate purposes.

🔸Co recently issued 24,340,771 Equity Shares through an IPO priced at ₹469 to ₹493 per share on December 13, 2023.

🔸The objective of issuing an IPO is to raise funds for future capital requirements towards onward lending and General corporate purposes.

✍️Industry Outlook:

🔸Housing finance credit outstanding as of March 31, 2023, was ₹31 lakh crore, with a 13.5% 4-year CAGR growth due to rising incomes and demand.

🔸The housing finance segment is expected to reach ₹47 lakh crore by FY26.

🔸Housing finance credit outstanding as of March 31, 2023, was ₹31 lakh crore, with a 13.5% 4-year CAGR growth due to rising incomes and demand.

🔸The housing finance segment is expected to reach ₹47 lakh crore by FY26.

🔸Public sector banks hold a 40% market share in housing loans, followed by HFCs at 34% in FY23.

🔸India's mortgage market has two segments: normal housing loans (>₹25 lakhs) and affordable housing loans (<₹25 lakhs), accounting for 37% of total credit.

🔸India's mortgage market has two segments: normal housing loans (>₹25 lakhs) and affordable housing loans (<₹25 lakhs), accounting for 37% of total credit.

✍️Key Strenghts:

🔸Diversified distribution of AUM with presence across 15 states.

🔸Co excels in combining physical and digital models, utilizing top-notch IT systems and technology to improve operations and customer experience.

🔸Diversified distribution of AUM with presence across 15 states.

🔸Co excels in combining physical and digital models, utilizing top-notch IT systems and technology to improve operations and customer experience.

🔸Growing demand for housing units due to increased urbanisation.

🔸Strong capital base backed by marquee investors.

🔸Strong capital base backed by marquee investors.

✍️Key Risks:

🔸63% of AUM is concentrated in Rajasthan, Maharashtra, and Madhya Pradesh; adverse events in these regions could impact the company's business operations.

🔸Volatility in the financial market.

🔸Increasing competition from existing as well as new players.

🔸63% of AUM is concentrated in Rajasthan, Maharashtra, and Madhya Pradesh; adverse events in these regions could impact the company's business operations.

🔸Volatility in the financial market.

🔸Increasing competition from existing as well as new players.

🔸Co targets first-time home loan customers in smaller Indian cities, which may have a higher risk of nonpayment or default.

🔸Co mainly serves low to middle-income customers with 71% self-employed and 29% salaried, facing default risks from various factors.

🔸Co mainly serves low to middle-income customers with 71% self-employed and 29% salaried, facing default risks from various factors.

✍️Future Outlook:

🔸Company's focus on customer satisfaction drives long-lasting relationships.

🔸Co expects a CAGR of 20.58% between 2022 and 2027 for the housing finance market.

🔸It is expected to reach ₹ 64.34 trillion by FY 2026-27.

🔸Company's focus on customer satisfaction drives long-lasting relationships.

🔸Co expects a CAGR of 20.58% between 2022 and 2027 for the housing finance market.

🔸It is expected to reach ₹ 64.34 trillion by FY 2026-27.

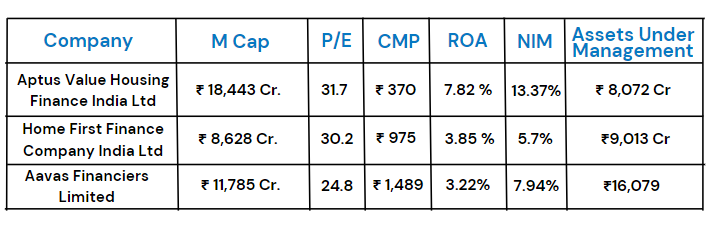

✍️Peer:

🔸Aptus Value Housing Finance India Ltd

🔸Aavas Financiers Ltd

🔸Home First Finance Company India Ltd

🔸Aptus Value Housing Finance India Ltd

🔸Aavas Financiers Ltd

🔸Home First Finance Company India Ltd

✍️Shareholding Pattern:

🔸Promoters: 48.30%

🔸FIIs: 5.84%

🔸DIIs: 12.61%

🔸Retailers: 33.24%

🔸Promoters: 48.30%

🔸FIIs: 5.84%

🔸DIIs: 12.61%

🔸Retailers: 33.24%

⚡️Disclaimer: The above data should not be considered as a Buy or Sell recommendation. The analysis has been done for educational and learning purpose only.

✅Follow <@raghavwadhwa> for more insights on Micro cap companies and various sectors.

✅Like & Retweet♻️

✅Visit our website samarwealth.com

✅Like & Retweet♻️

✅Visit our website samarwealth.com

Loading suggestions...