Through a series of patchwork FTAs, China is building a "backup" trading system to the WTO.

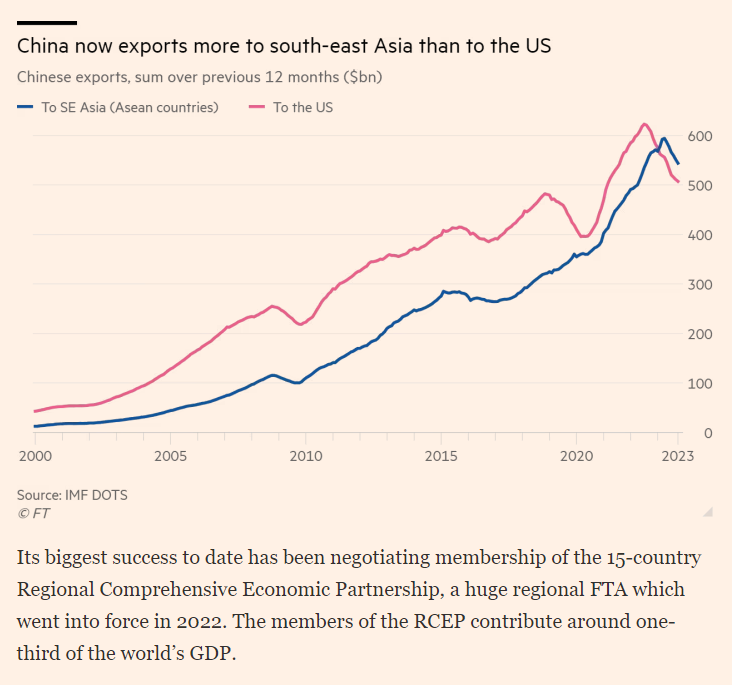

▪️ RCEP is the largest one, covering much of ASEAN/APAC.

▪️ FTAs are also in the works with the Middle East (GCC) and Africa (AfCFTA).

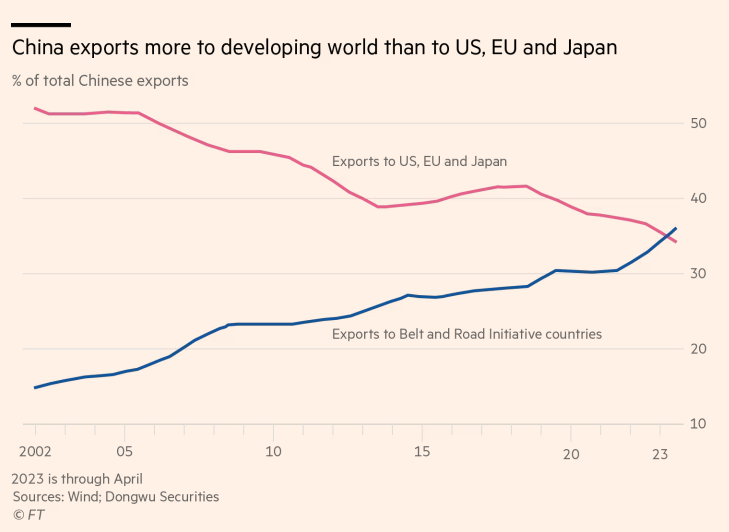

Many of these FTAs overlap with BRI.

▪️ RCEP is the largest one, covering much of ASEAN/APAC.

▪️ FTAs are also in the works with the Middle East (GCC) and Africa (AfCFTA).

Many of these FTAs overlap with BRI.

China "does not wish to see the demise of globalisation as represented by the WTO" but also does not pin its MT/LT development goals on trading relationships that are largely out of its control (e.g. rising protectionist sentiment in the US & EU).

"Trade losses" w/ the US & EU have been partly mitigated by rising intermediate trade with "neutral" third-party economies through either transshipment or real offshoring of "industrialization 1.0" labor-intensive consumer goods to countries likes Mexico, Malaysia and Vietnam.

Meanwhile these new FTA agreements, largely with the developing world, ensure that "industrialization 2.0" advanced manufacturing exports — categories like EVs, batteries and clean energy — are flowing disproportionately to the developing world.

Global trade dynamics are accelerating what had already been the LT dynamic of China's economy shifting from labor-intensive & low-capex manufacturing ("v1.0") to R&D/capex-intensive manufacturing ("v2.0").

This LT dynamic also follows China's underlying demographic transition from a largely blue-collar labor force (construction, labor-intensive manufacturing) to a white-collar (R&D and high-value services) college-educated one.

The largely blue-collar rural and migrant labor force is already shrinking and the decline will only accelerate into the 2030s with the peak mid-80s cohort hitting retirement.

This will have significant macro implications.

Chinese FX policy for decades has been oriented around a weak ¥, which fosters persistent trade surpluses that effectively result in the import of productive jobs ("gainful employment") from RoW.

Chinese FX policy for decades has been oriented around a weak ¥, which fosters persistent trade surpluses that effectively result in the import of productive jobs ("gainful employment") from RoW.

This was core policy b/c China was structurally over-supplied with non-productive labor since the beginning of its reforms.

Chinese policymakers recognized the spillover human capital benefits of "gainful employment" that went beyond the trade benefits.

Chinese policymakers recognized the spillover human capital benefits of "gainful employment" that went beyond the trade benefits.

And upgrading human capital is core to the MT and LT development goals enshrined in decades worth of 5YPs, namely achieving a "medium level of development by the late 2020s" and a "high-level of development by the 2040s".

As this structural labor over-supply situation reverses over the next 10-15 years, it is reasonable to assume major changes in these policies.

I expect that China will flip from a weak ¥ policy to a neutral or even strong ¥ stance in the coming decade or two.

I expect that China will flip from a weak ¥ policy to a neutral or even strong ¥ stance in the coming decade or two.

As domestic labor reaches full gainful employment (w/ urbanization rates as one of the key progress indicators), Chinese policy will begin to favor the import of labor from lower-income countries and economies.

This "import" of labor is more likely to take the form of offshoring of the most labor-intensive segments of the industrial value chain in the form of outbound Chinese FDI that maintains close links to the Chinese supply chain, particularly for more tech/R&D-intensive components.

In other words, China will be trading domestic technology, IP and know-how for labor, which is the position in the global value chain long held by developed OECD economies.

Strong ¥ policy favors this position.

Strong ¥ policy favors this position.

The other major macro shift will be China transitioning from being a major net importer of energy, primarily petroleum, to potentially a net energy exporter, driven by the clean energy transition.

Examining the current snapshot of China's petroleum usage provides clues in how this energy transition will happen.

First, transport electrification with passenger vehicles reduces gasoline demand (representing 20-25% of usage) over the next 10-15 years.

First, transport electrification with passenger vehicles reduces gasoline demand (representing 20-25% of usage) over the next 10-15 years.

Second, transport electrification with commercial trucks reduces diesel demand (~20% of usage) over the next two decades.

Third, green hydrogen (generated by excess renewables) begans to replace many industrial use cases, or certain industries are offshored (per above).

Third, green hydrogen (generated by excess renewables) begans to replace many industrial use cases, or certain industries are offshored (per above).

Fourth, electrification of residential heating reduces residential usage.

Fifth, heavy investments in HSR mitigate growth in kerosene/jet fuel usage (~6%) 👇

Fifth, heavy investments in HSR mitigate growth in kerosene/jet fuel usage (~6%) 👇

At this point, China's domestic petroleum production would be able to supply the majority, if not all of its petroleum needs.

(this will have significant effects on its trading relationships with resource-intensive economies like Russia and the ME)

(this will have significant effects on its trading relationships with resource-intensive economies like Russia and the ME)

Meanwhile, China's rapid expansion of clean energy manufacturing suggests that it is not just trying to replace coal in the grid, but to tap into the vast potential of what is effectively an unlimited energy source.

Driven by rapidly declining per-unit costs in both solar and wind, China has smashed through its own long-term goals for solar and wind deployment.

Net-zero is likely going to arrive sooner than expected.

Net-zero is likely going to arrive sooner than expected.

Even more significantly, that China will soon start generating more clean energy than it needs.

Converting this excess clean energy into different forms requires multiple "offtake" options.

Green hydrogen is one of them.

Converting this excess clean energy into different forms requires multiple "offtake" options.

Green hydrogen is one of them.

When I say China will become a net energy exporter, this could take many forms.

Direct electricity exports are likely only a small component of this.

More likely, it will take indirect forms, like how cheaper energy can shift absolute economic advantages.

Direct electricity exports are likely only a small component of this.

More likely, it will take indirect forms, like how cheaper energy can shift absolute economic advantages.

Historically, energy and labor were the two main constraints on economic growth:

▪️ Near-unlimited clean energy removes the energy constraint.

▪️ AI could be the solution to the labor constraint.

These two trends potentially open the door to the "Post-Abundance" economy.

▪️ Near-unlimited clean energy removes the energy constraint.

▪️ AI could be the solution to the labor constraint.

These two trends potentially open the door to the "Post-Abundance" economy.

Loading suggestions...