Global containerized ocean freight prices are surging to levels not seen since the pandemic supply chain crunch. Some key trade lane rates are up 140% since mid-December and increasing by the week. What’s happening, why, and what it means for businesses needing products moved? 🧵

The simplest answer for why prices are surging is that freight is one of the most inelastic markets in the entire global economy—brands rarely ship more stuff just because the price of freight is cheap, or less stuff because the price of freight is expensive.

In a competitive market with inelastic demand, when demand for shipping goods exceeds the supply of the world's cargo-carrying capacity, the price will increase to the rate that those are most willing to pay to get them moved.

Starting last December, terrorist attacks in the Red Sea forced the world's container ships to divert around Africa, reducing shipping capacity. That's because it takes 30-40% longer to complete the round trip from Asia to Europe, lowering the network's effective throughput.

To put this into perspective, the Shanghai Containerized Freight Index (SCFI), which measures the containerized freight price in the spot market, is surging. Shanghai to Europe rates hit $3050/TEU - a 155% increase from April 15, and nearly 3x increase from Dec 15, 2023

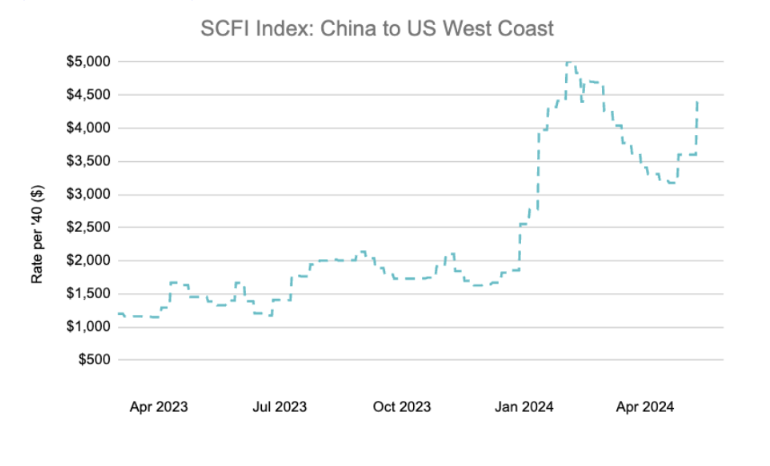

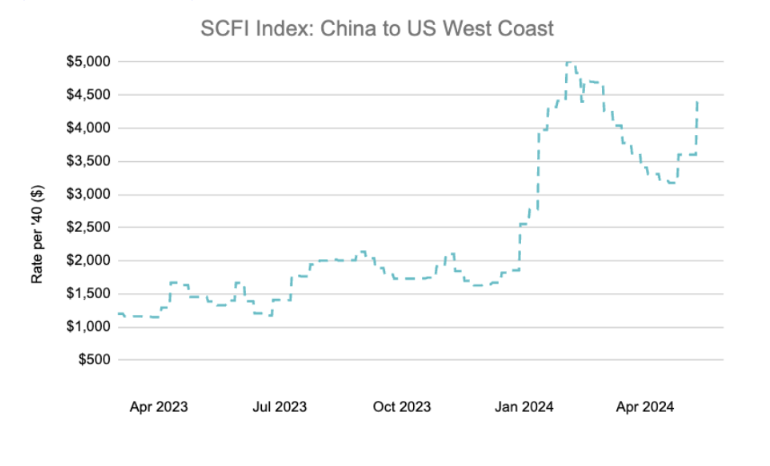

The Asia to US trade lanes have also been heavily impacted, with rates from Shanghai to the US West Coast hitting $4,393 - a 37% increase from April 15, and a 142% increase from Dec 15, 2023.

But wait, why are transpacific trade lanes impacted by the Asia to Europe trade capacity reductions? To compensate for capacity gaps caused by the Suez reroutings, carriers rotated many ships from the Pacific to Asia-Europe lanes.

Also, in mid-April port congestion surged with poor weather—heavy fog in two of China’s biggest ports Shanghai and Ningbo, along with heavy rain in Malaysia and Singapore. Global shipping is a chaotic system in the literal sense as it depends on the weather and even the earth’s geology (volcanos etc)

The North American market is grappling with its own issues. A potential Canadian rail strike this month is scaring importers from the fastest route to the Midwest from the Pacific (rail from Prince Rupert down to Chicago), pushing them to move goods through US gateways instead.

Problems are worse on the US East Coast with a near-perfect storm of disruption. First, the fastest route to the East Coast from South Asia and the Middle East is through the Suez. Ships on those lanes must go around Africa or cross the Pacific and go through the Panama Canal.

But the Panama Canal has been suffering from lack of water. It's been limited to 2/3 capacity during a drought (effectively its pre-2015 capacity), and recovery has been slow.

Adding to problems for East Coast ports is the Baltimore disaster where the Maersk MV Dali collapsed the Key Bridge and cut the U.S. ninth busiest port’s access to the global ocean for over a month.

Perhaps worst for shippers moving cargo to the East Coast is that the International Longshoreman Association (ILA), the union operating all ports on the East and Gulf Coasts, has a contract expiring on Sept 30. Talks are ongoing and wage increase will likely be a sticking point.

Map of ports operated by the ILA (ilaunion.org)

Map of ports operated by the ILA (ilaunion.org)

Strike or not, shippers are nervous about delays mere weeks before the peak holiday shipping season (cargo typically gets to port before Black Friday starts holiday shopping season). Companies fear they may miss Christmas if cargo doesn't get into East Coast ports before Sept 30.

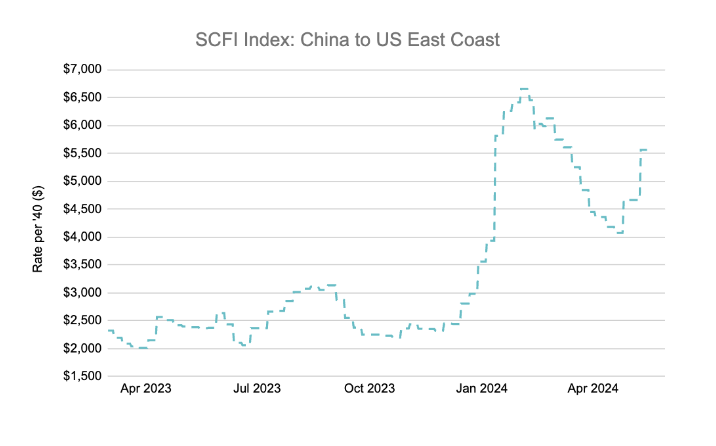

That pull forward of demand is coming at the same time as capacity is severely constrained, leading to a surge in US east coast rates too: Shanghai to the US East Coast on the index hitting $5562 - a 33% increase from April 15, and a 98% increase from Dec 15, 2023.

With spot market rates soaring over rates on annual fixed contracts, many contracts are now running into challenges in getting fulfilled. Almost all fixed-rate contracts are subject to a “peak season surcharge” (PSS) implemented at the carrier’s discretion. In this market the shipper won't pay, they won't get loaded.

flexport.com

flexport.com

As of this month, all ocean carriers and forwarders have applied a PSS to almost all fixed-rate contracts, even ones signed weeks ago. The PSS has elevated the fixed-rate prices, sometimes bringing them close to the spot market rates, which may be 2 to 3 times higher.

Shippers, especially those with fixed rate contracts, are naturally unhappy about the price surge. If they believe prices will go up in the future, they’ll push hard for inventory to move on earlier departures, leading to still more capacity issues in a compounding feedback loop and even panic bookings.

Ocean carriers are pushing “premium” options as a method to get cargo prioritized on the first available departure date with higher equipment priority, though at a higher cost. This approach is one of the only options right now to avoid delays and ensure timely deliveries.

Why did nobody see this coming? Shipping is full of black swans: terrorism, bridge collapses, labor union unrest, intense weather, and more. Forecasting them accurately is nearly impossible. Even after they occur, their second and third order effects are hard to predict.

Many experts thought that new ships built since COVID would be enough to overcome the supply shock from longer routing around Africa. Such calculations are generally aggregated, ignoring the granularity of available capacity on a given day, sailing, and port pair customers require.

What’s next? Short term, firms have to accept the market reality. Many will complain but the reality is ocean carriers are capital intensive businesses. The life cycle of these ships is 20-30 years, so at the time they're bought, carriers have no idea what demand will look like, much less the black swans.

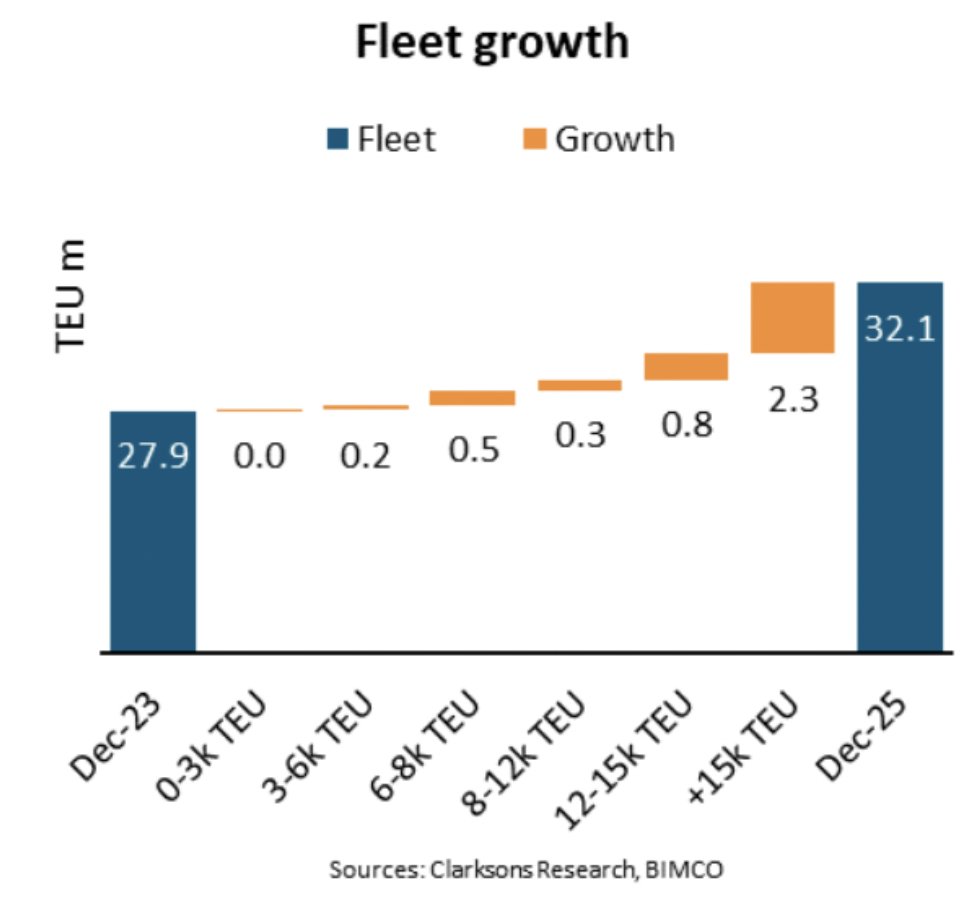

We should also remember that high prices are a signal for carriers to invest in more container ships, which they’ve done in spades since Covid. Thanks to those reinvestments, ocean container shipping capacity is expected to increase significantly since the 2022 supply chain crisis began to unwind. There's millions of TEUs more capacity of container shipping coming online in the next few years:

While it’s tempting to compare the current market to the Covid capacity crunch, this is different. The pandemic price surge—with the spot rates regularly reaching up to $20K per container on the US West Coast – was largely caused by an enormous spike in consumer demand.

Rather the current capacity crunch is supply-driven. I don’t know when the Red Sea will be deemed safe again, but we can say with reasonable confidence that carriers hope that new ships being delivered into 2026 should service the capacity eliminated by the rerouting and other disruptions.

Remember Nassim Taleb: “I’ve never seen a shortage not followed by a glut.”

It’s only a matter of time before we’re back to a world of excess capacity and I promise you, we won’t find a single company offering to pay more to help the carriers out.

It’s only a matter of time before we’re back to a world of excess capacity and I promise you, we won’t find a single company offering to pay more to help the carriers out.

Then again, I had thought we’d already be in that world by now. Even as recently as two months ago I predicted there would be plenty of capacity to overcome the Red Sea reroutings. By now I should know that in global shipping there’s always another disruption around the corner.

Rather than focusing on predicting the future, the best advice for global logistics professionals is to stay agile and ready for whatever the world throws at you. Observe, orient, decide, act, and repeat. Agility is the name of the game to stay ahead in the ever-changing world of shipping and logistics.

Uncertain, volatile situations like this create competitive advantage for those who are best at responding to the chaos. As my father used to say on our camping trips, "you don't have to outrun the bear, just the slowest camper."

Loading suggestions...