Setting up a Solo 401k is the biggest personal finance win for anyone self-employed

- A $69K tax deduction per spouse

- Tax-free compounding

- Support for Roth contributions

- Invest in any asset class

- $1500 tax credit for setting one up

- Borrow up to $50K from your plan 👇

- A $69K tax deduction per spouse

- Tax-free compounding

- Support for Roth contributions

- Invest in any asset class

- $1500 tax credit for setting one up

- Borrow up to $50K from your plan 👇

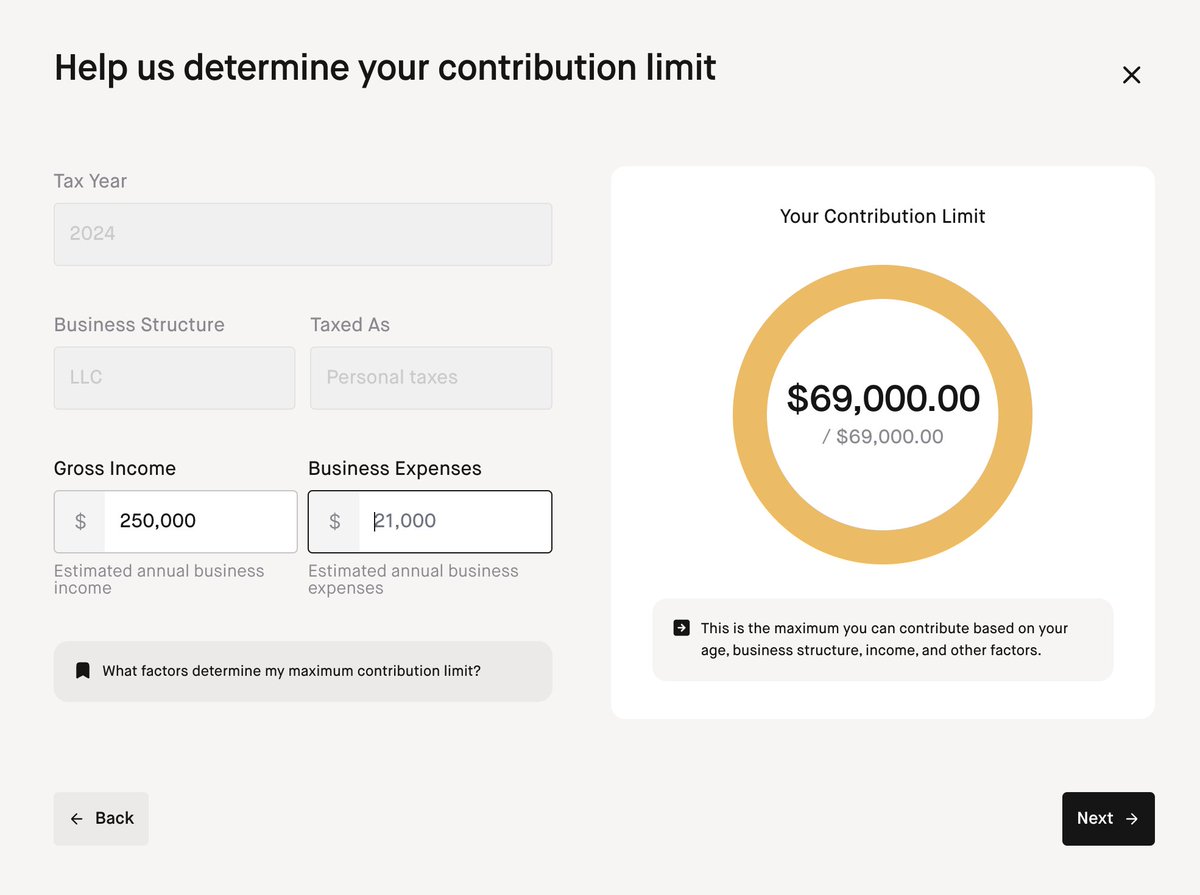

1) $69K Tax Deduction

You can contribute as an employer & employee and get up to a $69K tax deduction

If your spouse works at the business, you each get your own $69K upper limit & can double it

If you are over 50, this increases to $76,500!

You can contribute as an employer & employee and get up to a $69K tax deduction

If your spouse works at the business, you each get your own $69K upper limit & can double it

If you are over 50, this increases to $76,500!

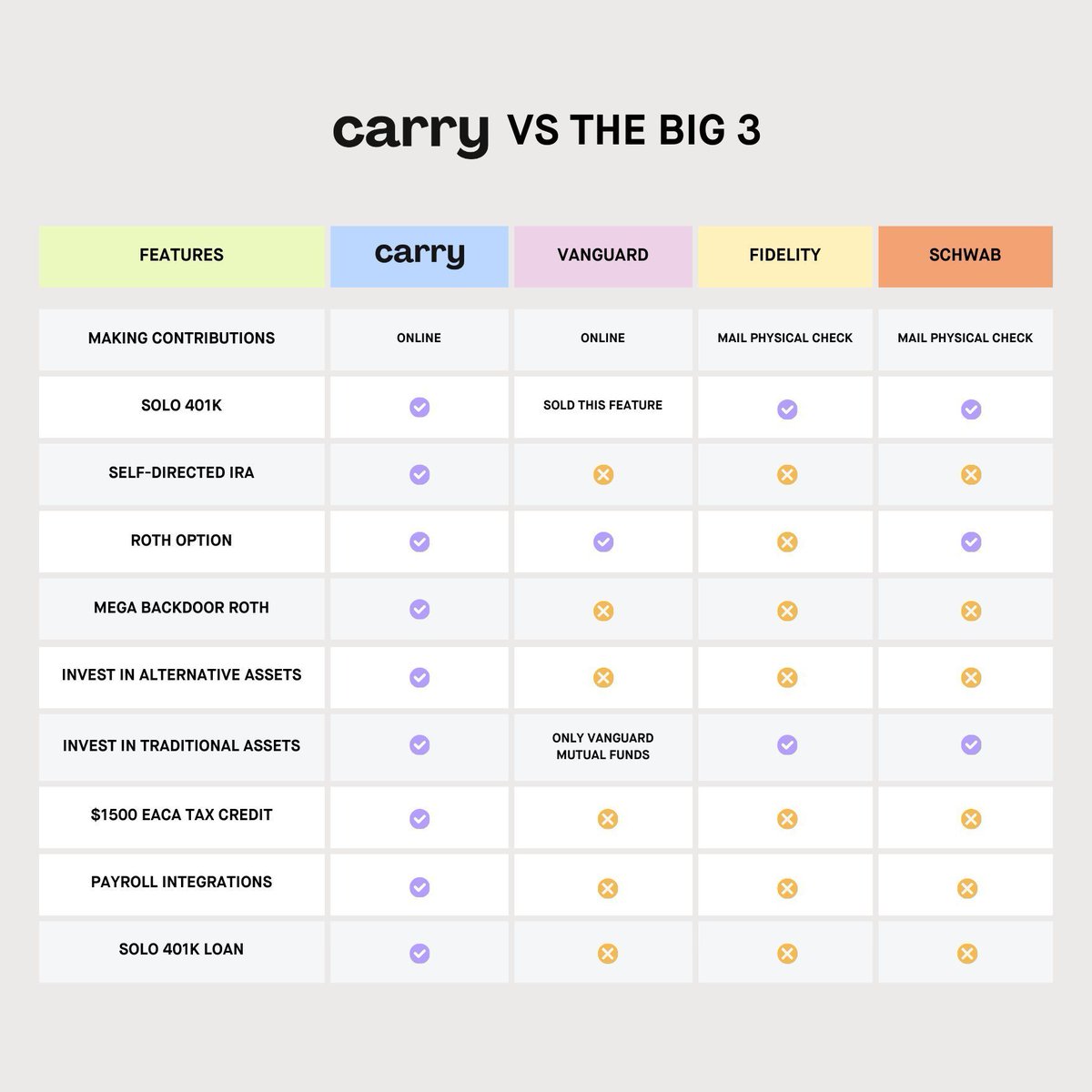

2) Invest in Anything

Unlike your corporate 401k plan, you can self-direct this plan to invest in any asset class you would like

Mutual funds, individual stocks or ETF's -- or startups, private equity, venture funds & real estate

Unlike your corporate 401k plan, you can self-direct this plan to invest in any asset class you would like

Mutual funds, individual stocks or ETF's -- or startups, private equity, venture funds & real estate

3) Tax-Free Compounding

All the growth in the account is entirely tax-free

Dividends, buying and selling securities, rent payments (for commercial real estate)

All entirely tax-free. You only pay taxes when you withdraw funds in retirement unless you decide to do...

All the growth in the account is entirely tax-free

Dividends, buying and selling securities, rent payments (for commercial real estate)

All entirely tax-free. You only pay taxes when you withdraw funds in retirement unless you decide to do...

4) Roth Contributions

Solo 401k's also support Roth contributions which would make all your earnings entirely tax-free in retirement

You can also do a mega-backdoor Roth to make the entire $69,000 contribution as a Roth contribution

And repeat it every single year

Solo 401k's also support Roth contributions which would make all your earnings entirely tax-free in retirement

You can also do a mega-backdoor Roth to make the entire $69,000 contribution as a Roth contribution

And repeat it every single year

5) Borrow Money from Your Plan

If you need to access the money before you retire, you can always take a loan from your Solo 401k

You can borrow up to the maximum of $50K or 50% of your total account value

The best part? The interest you pay goes right back into your plan!

If you need to access the money before you retire, you can always take a loan from your Solo 401k

You can borrow up to the maximum of $50K or 50% of your total account value

The best part? The interest you pay goes right back into your plan!

6) Get a $500 Tax Credit for 3 Years for Setting One Up

When you set up a Solo 401k, use a provider that lets you enable automatic contributions on the plan (like @carryhq_ )

This makes you eligible for a $500 EACA tax credit for 3 years ($1500 total)

Free money!

When you set up a Solo 401k, use a provider that lets you enable automatic contributions on the plan (like @carryhq_ )

This makes you eligible for a $500 EACA tax credit for 3 years ($1500 total)

Free money!

Who is eligible for a Solo 401k?

Anyone who is self-employed or owns a business with no W-2 employees (excluding your spouse or other business owners)

If you have a full-time W-2 job, but have a side hustle, you can set up a Solo 401k with your side hustle

Anyone who is self-employed or owns a business with no W-2 employees (excluding your spouse or other business owners)

If you have a full-time W-2 job, but have a side hustle, you can set up a Solo 401k with your side hustle

Why set up a Solo 401k vs a SEP IRA?

- You can put more $ into a Solo 401k since you can make employer & employee contributions

- Better support for Roth contributions

- Can borrow money from your plan

- Catch-up contributions if over 50

- Makes a backdoor Roth IRA easier

- You can put more $ into a Solo 401k since you can make employer & employee contributions

- Better support for Roth contributions

- Can borrow money from your plan

- Catch-up contributions if over 50

- Makes a backdoor Roth IRA easier

Want a demo of the Carry Solo 401k platform?

DM me and I'll walk you through it

And we're also doing a bigger public walkthrough at 2pm ET today, sign up here: streamyard.com

Will also send a replay

DM me and I'll walk you through it

And we're also doing a bigger public walkthrough at 2pm ET today, sign up here: streamyard.com

Will also send a replay

Loading suggestions...