Do Indians require a bigger retirement corpus than Americans?

To plan your retirement, many may tell you to follow the 25X corpus rule.

This rule originated in the US and works well for Americans.

But it may not work in India.

Here’s why. A thread🧵

To plan your retirement, many may tell you to follow the 25X corpus rule.

This rule originated in the US and works well for Americans.

But it may not work in India.

Here’s why. A thread🧵

25X Rule Simplified

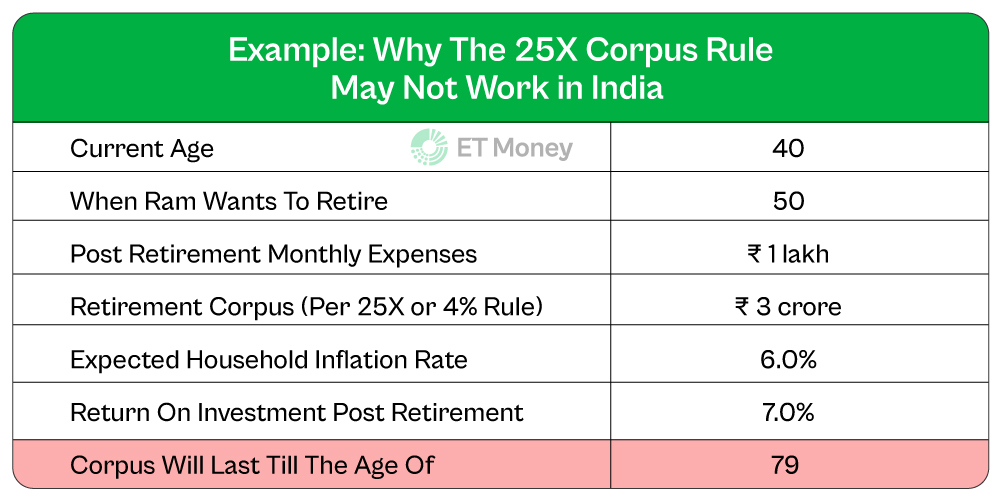

Say, 40-year-old Ram wants to retire at 50.

He thinks his post-retirement expenses will be ₹12 lakh a year.

Per the 25X rule, Ram needs 25 times of Rs 12 lakh (i.e., Rs 3 crore) to retire.

What’s the logic behind this rule?

Say, 40-year-old Ram wants to retire at 50.

He thinks his post-retirement expenses will be ₹12 lakh a year.

Per the 25X rule, Ram needs 25 times of Rs 12 lakh (i.e., Rs 3 crore) to retire.

What’s the logic behind this rule?

The 25x rule is a twist on the 4% rule.

In 1994, advisor William Bengen found that withdrawing 4% annually from retirement savings could last at least 30 years after retirement.

This boiled down to saving 25 times your yearly expenses for financial freedom.

But, the rule may not work in india.

In 1994, advisor William Bengen found that withdrawing 4% annually from retirement savings could last at least 30 years after retirement.

This boiled down to saving 25 times your yearly expenses for financial freedom.

But, the rule may not work in india.

Let’s go back to Ram’s example.

Say, he has ₹3 crore to retire.

In the first year, Ram will withdraw 4% (₹2 lakh).

Next year, assuming 6% inflation, he will need to withdraw ₹12.72 lakh (4.24% of ₹3 cr).

Every year, the withdrawal rate will keep increasing due to inflation.

Say, he has ₹3 crore to retire.

In the first year, Ram will withdraw 4% (₹2 lakh).

Next year, assuming 6% inflation, he will need to withdraw ₹12.72 lakh (4.24% of ₹3 cr).

Every year, the withdrawal rate will keep increasing due to inflation.

Now, say Ram invests his corpus. Earns a 7% return every year.

Even then, he will run out of savings in his late 70s.

Even then, he will run out of savings in his late 70s.

Why this 25X corpus rule doesn’t work in India?

US financial planner William P. Bengen created the 4% rule in the 1990s.

He did the calculation based on inflation in the US.

But in India, inflation is much higher.

That’s why the rule is unlikely to work here.

US financial planner William P. Bengen created the 4% rule in the 1990s.

He did the calculation based on inflation in the US.

But in India, inflation is much higher.

That’s why the rule is unlikely to work here.

What Can You Do?

There are two ways to approach early retirement with 4% rule:

Stick to the 4% rule. Take semi-retirement. Work part-time.

If you prefer not to work at all, aim to save more. Like 35X or 40X your annual post-retirement expenses.

There are two ways to approach early retirement with 4% rule:

Stick to the 4% rule. Take semi-retirement. Work part-time.

If you prefer not to work at all, aim to save more. Like 35X or 40X your annual post-retirement expenses.

Loading suggestions...