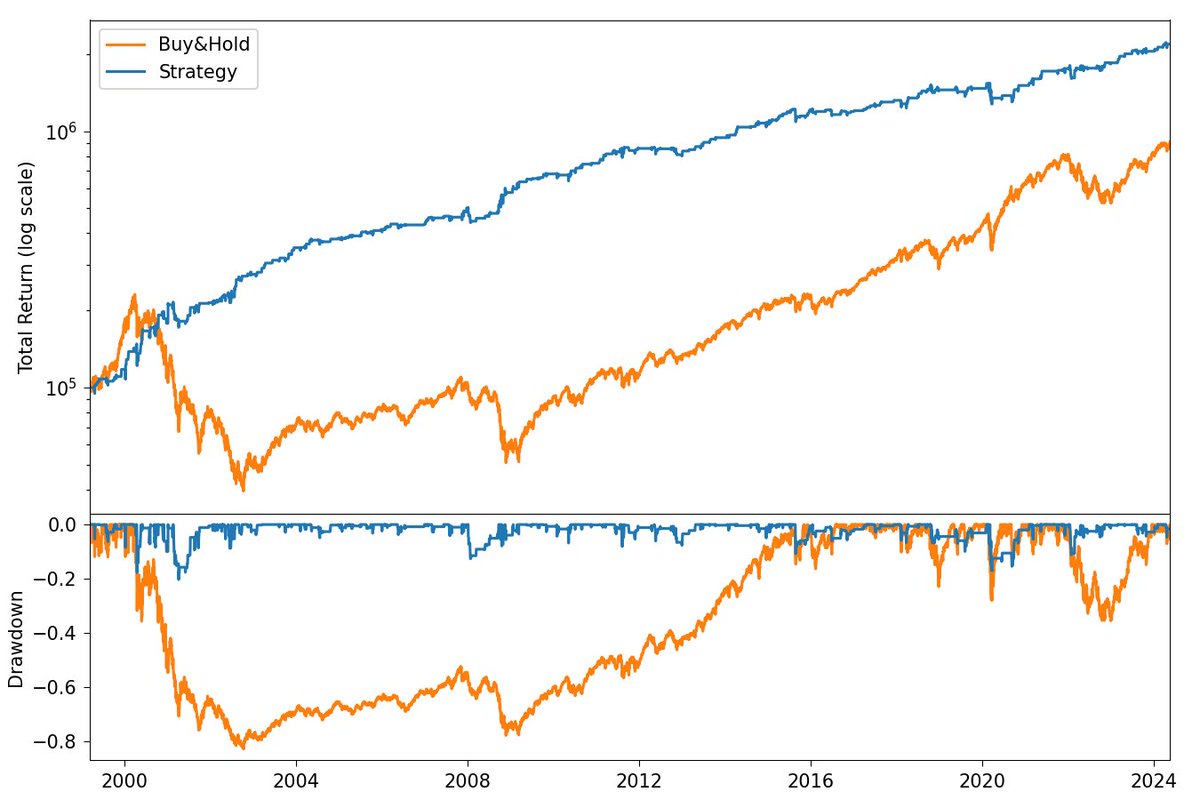

A 2.11 Sharpe mean-reversion strategy:

- More than 3x the return of S&P 500 and ~1.5x Nasdaq-100 since 1999

- 20% max drawdown vs. 57% S&P 500 and 83% Nasdaq-100

- 16 trades/year @ 69% win rate

🧵Here's how it works:

- More than 3x the return of S&P 500 and ~1.5x Nasdaq-100 since 1999

- 20% max drawdown vs. 57% S&P 500 and 83% Nasdaq-100

- 16 trades/year @ 69% win rate

🧵Here's how it works:

Signals:

- Compute the rolling mean of High minus Low over the last 25 days;

- Compute the IBS indicator: (Close - Low) / (High - Low);

- Compute a lower band as the rolling High over the last 10 days minus 2.5 x the rolling mean of High mins Low

- Compute the rolling mean of High minus Low over the last 25 days;

- Compute the IBS indicator: (Close - Low) / (High - Low);

- Compute a lower band as the rolling High over the last 10 days minus 2.5 x the rolling mean of High mins Low

Entry rule:

Go long whenever SPY closes under the lower band (3rd bullet), and IBS is lower than 0.3

Exit rule:

Close the trade whenever the SPY close is higher than yesterday's high

All the implementation details:

quantitativo.com

Go long whenever SPY closes under the lower band (3rd bullet), and IBS is lower than 0.3

Exit rule:

Close the trade whenever the SPY close is higher than yesterday's high

All the implementation details:

quantitativo.com

Loading suggestions...