Last month, OYO withdrew its IPO papers

And is now raising a round at a $2.5 Bn valuation, down 75% from its peak $10 Bn valuation back in 2019

The crazy part? The company just posted its first annual net profit of ₹100 Cr!

THREAD: How OYO’s profitability hurt its valuation🧵

And is now raising a round at a $2.5 Bn valuation, down 75% from its peak $10 Bn valuation back in 2019

The crazy part? The company just posted its first annual net profit of ₹100 Cr!

THREAD: How OYO’s profitability hurt its valuation🧵

The famous branded network of hotels, OYO, was valued at a staggering $10 billion in 2019 and clocked its first ever profitable year in FY24.

So, what caused OYO's valuation to be slashed by over 75% to just $2.3 billion, even though it finally turned profitable?

So, what caused OYO's valuation to be slashed by over 75% to just $2.3 billion, even though it finally turned profitable?

OYO initially positioned itself as an affordable hotel brand with great service.

For a traveler on a short stay, it was a no-brainer to book an OYO room due to its assured quality.

But over time, OYO began losing credibility in its quality while fixating on affordability.

For a traveler on a short stay, it was a no-brainer to book an OYO room due to its assured quality.

But over time, OYO began losing credibility in its quality while fixating on affordability.

One thing about the Indian hospitality customer is that they cannot compromise on basic hotel quality.

An excellent example would be WOW! Momo.

See, momos are made the same by every vendor but WOW! Momo ensures its quality so the customer can rest assured.

OYO operated similarly — offering exactly what every other budget hotel did, but the ‘OYO seal’ was quality assurance.

See, momos are made the same by every vendor but WOW! Momo ensures its quality so the customer can rest assured.

OYO operated similarly — offering exactly what every other budget hotel did, but the ‘OYO seal’ was quality assurance.

When this quality was compromised, OYO got stereotyped as a ‘love hotel’ which drove many of its customers away due to its fall in reputation,

especially in Indian society where such association is heavily frowned upon.

especially in Indian society where such association is heavily frowned upon.

But this took a turn during the pandemic when the hospitality industry took the biggest economic blow and OYO’s survival depended on turning profitable.

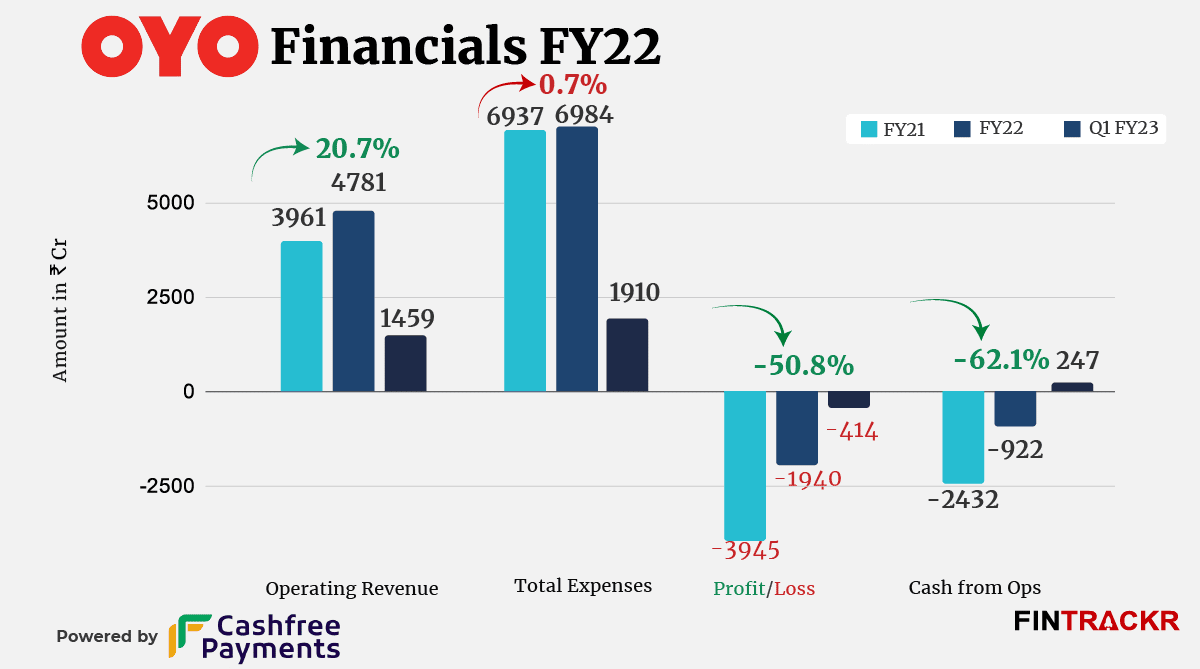

OYO's revenue dropped by 70%, going from ₹13,000 Cr to just ₹4,000 Cr in 2021.

OYO's revenue dropped by 70%, going from ₹13,000 Cr to just ₹4,000 Cr in 2021.

This forced the company to prioritize customer satisfaction and quality over market expansion, and adopt a more conservative financial approach to their operational expenditure.

To achieve this, OYO decreased its number of hotels to 12,938 in FY23 from 18,037 in FY22.

To achieve this, OYO decreased its number of hotels to 12,938 in FY23 from 18,037 in FY22.

The company even emptied its headquarters in Gurugram, laid off employees, and even exited loss-making ventures like ‘OYO Life’ as a cost-cutting measure.

Not just that, OYO claims that their technological integration and support also immensely helped in bringing the costs down.

Not just that, OYO claims that their technological integration and support also immensely helped in bringing the costs down.

These efforts, plus programs like ‘Spotless Stays’ and ‘Super OYO’, raised customer satisfaction,

leading OYO to go from ₹2000 crores in losses to the first fiscal net profit of ₹100 crores in FY23-24.

leading OYO to go from ₹2000 crores in losses to the first fiscal net profit of ₹100 crores in FY23-24.

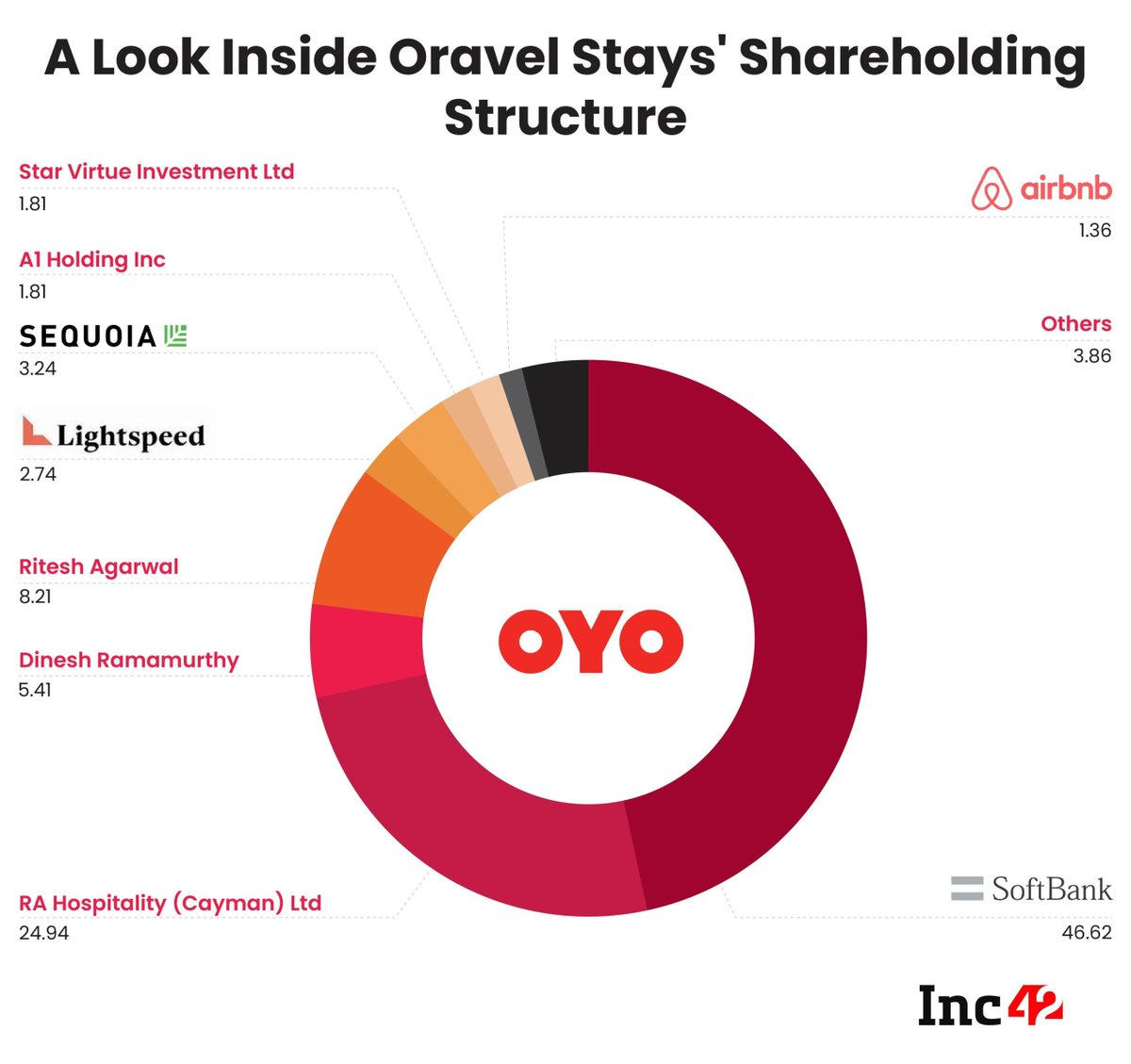

But even with these great projections, in 2022, OYO’s valuation had been slashed to $2.7 Bn by SoftBank, which holds a 46% stake.

And most recently, OYO is raising ₹1000 crore from family offices at an even lower valuation of $2.5 Bn after withdrawing their 2nd IPO application.

And most recently, OYO is raising ₹1000 crore from family offices at an even lower valuation of $2.5 Bn after withdrawing their 2nd IPO application.

But why would a company’s valuation continue to decline if it has finally managed to turn profitable?

Well, OYO’s decision to save its business through profitability could also have been the very reason that made its valuation suffer.

Well, OYO’s decision to save its business through profitability could also have been the very reason that made its valuation suffer.

See, investors initially trusted OYO’s limitless potential and hunger for aggressive market penetration.

But they realized the limitations as OYO only became profitable after suffering a funding drought and reducing its operations

— the scarcity actually improved the business.

But they realized the limitations as OYO only became profitable after suffering a funding drought and reducing its operations

— the scarcity actually improved the business.

But scarce operations are never good for valuations as investors tend to bet on aggressive market capitalisation.

This made the investors realise that OYO was not the all-pervasive hospitality monopoly that they had hoped for it to be.

This made the investors realise that OYO was not the all-pervasive hospitality monopoly that they had hoped for it to be.

Not just that, SoftBank’s hesitation in maintaining OYO’s valuation could have also been influenced by:

👉Shrunk TAM: Due to its tarnished image, OYO's target audience started to prefer competitors, & COVID-19 resulted in long-drawn turbulence in the travel & hospitality sector.

👉Shrunk TAM: Due to its tarnished image, OYO's target audience started to prefer competitors, & COVID-19 resulted in long-drawn turbulence in the travel & hospitality sector.

👉Inflated valuation: At its peak valuation, OYO operated in a money-cheap market, meaning that the abundance of capital let them wrongly estimate potential which led to significant capital burn.

This was seen as an aggressive start-up approach and created the illusion of limitless potential for OYO, leading to an overestimation of its valuation.

Essentially, there was no winning for OYO — its bet on survival became the bane of its valuation.

Essentially, there was no winning for OYO — its bet on survival became the bane of its valuation.

If you liked this read, do RePost🔄 the 1st post

and follow us @FinFloww for such reads every Monday, Wednesday and Friday!

and follow us @FinFloww for such reads every Monday, Wednesday and Friday!

Join 25087 people who read such stories daily on our WhatsApp Newsletter: whatsapp.com

Subscribe to WHAT THE FLOWW?, our email newsletter where we dive deeper into such concepts: soshals.app

Loading suggestions...