You need to understand this if you want to make money from options trading

A detailed 🧵on Monetizing the relationship between Skew and Term structure

A detailed 🧵on Monetizing the relationship between Skew and Term structure

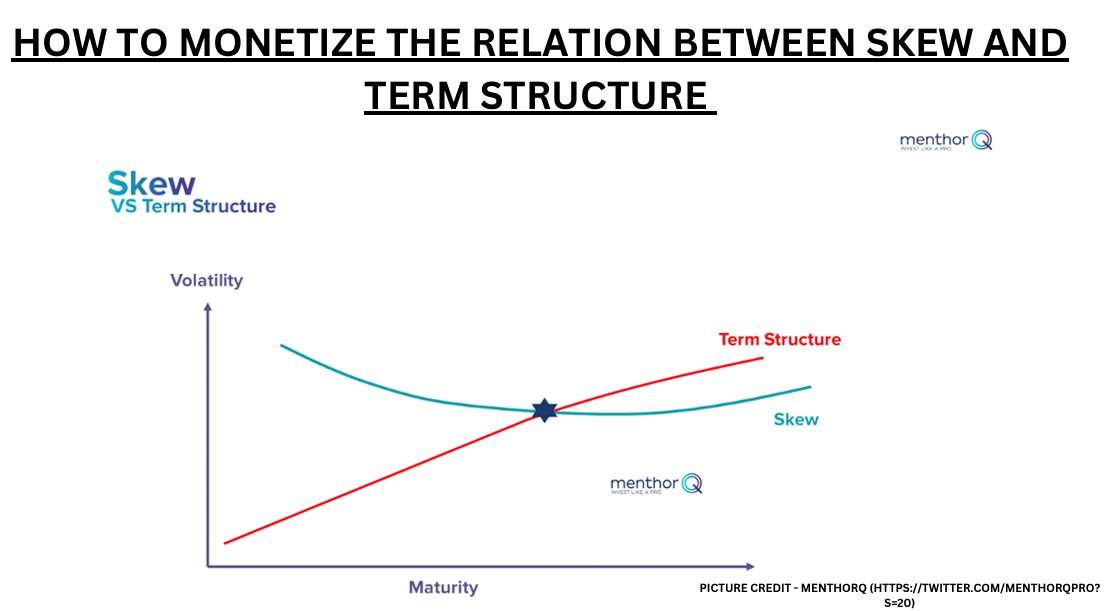

Skew and term structure are related in that a significant skew in one direction can affect the shape of the term structure.

The term structure can be defined as the relationship between implied volatility and time to expiration for options contracts.

The term structure can be defined as the relationship between implied volatility and time to expiration for options contracts.

In a left-skewed market, where out-of-the-money put options have a higher implied volatility than OTM call options, the term structure may be steeper on the left side (i.e. for options with lower strike prices and higher implied volatility levels) than on the right side.

This is because the skew makes put options more expensive, causing the implied volatility of shorter-term put options to be even higher relative to longer-term put options.

Here are some scenarios that can illustrate this:

Scenario 1

A left-skewed market with an upward-sloping term structure.

Suppose that a stock is trading at $100, and the implied volatility of out-of-themoney put options with a strike price of $90 is higher than that of

Scenario 1

A left-skewed market with an upward-sloping term structure.

Suppose that a stock is trading at $100, and the implied volatility of out-of-themoney put options with a strike price of $90 is higher than that of

out-of-the-money call options with a strike price of $110.

Additionally, the term structure is upwardsloping, meaning that longer-term options have higher implied volatility levels than shorter-term options.

Additionally, the term structure is upwardsloping, meaning that longer-term options have higher implied volatility levels than shorter-term options.

In this scenario, the skew is causing the left side of the term structure to be steeper than the right side. Options with lower strike prices (i.e., closer to the current market price) will have higher implied volatility levels than options with higher strike prices.

Furthermore, since the term structure is upward-sloping, this means that the skew effect is more pronounced for shorter-term options than for longer-term options.

Scenario 2: A left-skewed market with a flat term structure.

Now suppose that the term structure is flat, meaning that the implied volatility levels are relatively similar across different expiration dates

In this scenario, the skew effect may still be present,

Now suppose that the term structure is flat, meaning that the implied volatility levels are relatively similar across different expiration dates

In this scenario, the skew effect may still be present,

but it will be less pronounced since the term structure is not as steep. Options with lower strike prices will still have higher implied volatility levels than options with higher strike prices, but the difference between the two may not be as pronounced as in Scenario 1.

In a right-skewed market, where OTM call options have a higher implied volatility than out-of-the-money put options, the term structure may be steeper on the right side (i.e., for options with higher strike prices and lower implied volatility levels) than on the left side.

This is because the skew makes call options more expensive, causing the implied volatility of shorter-term call options to be even higher relative to longer-term call options

Scenario 3: A right-skewed market with an upward-sloping term structure.

Suppose that a stock is trading at $100, and the implied volatility of OTM call options with a strike price of $110 is higher than that of out-of-the money put options with a strike price of $90

Suppose that a stock is trading at $100, and the implied volatility of OTM call options with a strike price of $110 is higher than that of out-of-the money put options with a strike price of $90

Additionally, the term structure is upward-sloping, meaning that longer-term options have higher implied volatility levels than shorter-term options.

In this scenario, the skew is causing the right side of the term structure to be steeper than the left side. Options with higher strike prices will have lower implied volatility levels than options with lower strike prices.

Furthermore, since the term structure is upward-sloping, this means that the skew effect is more pronounced for shorter-term options than for longer-term options.

Scenario 4: A left-skewed market with a downward-sloping term structure.

Suppose that a stock is trading at $100, and the implied volatility of OTM put options with a strike price of $90 is higher than that of out-of-the money call options with a strike price of $110

Suppose that a stock is trading at $100, and the implied volatility of OTM put options with a strike price of $90 is higher than that of out-of-the money call options with a strike price of $110

Additionally, the term structure is downward-sloping, meaning that shorter-term options have higher implied volatility levels than longer-term options.

In this scenario, the skew is causing the left side of the term structure to be steeper than the right side, even though the overall term structure is downward sloping.

Options with lower strike prices will have higher implied volatility levels than options with higher strike prices, but this effect may be more pronounced for longer-term options than for shorter-term options.

Scenario 5: A right-skewed market with a downward-sloping term structure

Suppose that a stock is trading at $100 and the implied volatility of out-of-the money call options with a strike price of $110 is higher than that of out-of-the money put options with a strike price of $90

Suppose that a stock is trading at $100 and the implied volatility of out-of-the money call options with a strike price of $110 is higher than that of out-of-the money put options with a strike price of $90

Additionally, the term structure is downward-sloping, meaning that shorter-term options have higher implied volatility levels than longer-term options.

In this scenario, the skew is causing the right side of the term structure to be steeper than the left side, even though the overall term structure is downward-sloping.

Options with higher strike prices will have lower implied volatility levels than options with lower strike prices, but this effect may be more pronounced for longer term options than for shorter-term options.

Loading suggestions...