Pure drinking water is a need of billions not only in India but across the world🥤🥤

Va Tech Wabag is a market leader in the water treatment and purification space

A thread🧵 on the business of Va Tech Wabag and what lies ahead?

Lets go👇

Va Tech Wabag is a market leader in the water treatment and purification space

A thread🧵 on the business of Va Tech Wabag and what lies ahead?

Lets go👇

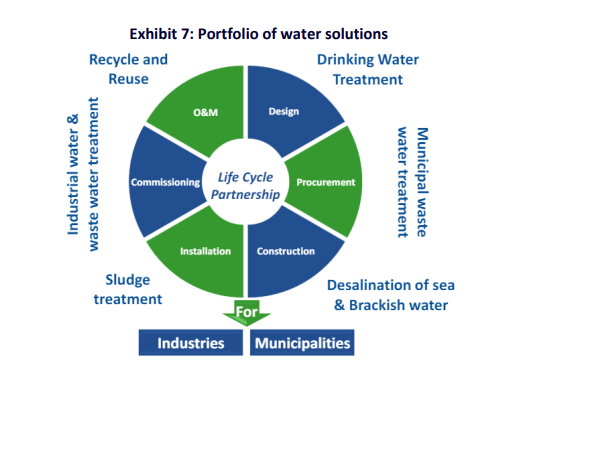

What is the business of Va Tech Wabag?

Va tech Wabag operates mainly in the Water treatment space

1. Recycle and reuse of water

2. Drinking Water Treatment

3. Desalination of sea and brackish water

4. Sludge treatment

Va tech Wabag operates mainly in the Water treatment space

1. Recycle and reuse of water

2. Drinking Water Treatment

3. Desalination of sea and brackish water

4. Sludge treatment

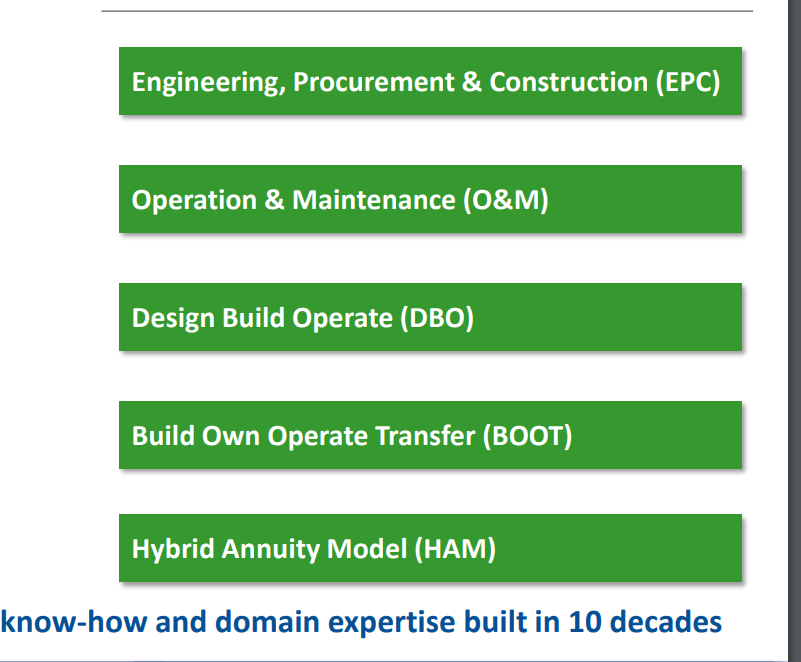

The company operates in the asset light model under the following ways

1. EPC model

2. Operate and Maintainance

3. Design build and Operate

4. Build own and transfer

5. Hyodib annuity mode

1. EPC model

2. Operate and Maintainance

3. Design build and Operate

4. Build own and transfer

5. Hyodib annuity mode

Clients:-

Va tech works with clients in India as well as abroad.

They also work with Municipal corporation within a city

Va tech works with clients in India as well as abroad.

They also work with Municipal corporation within a city

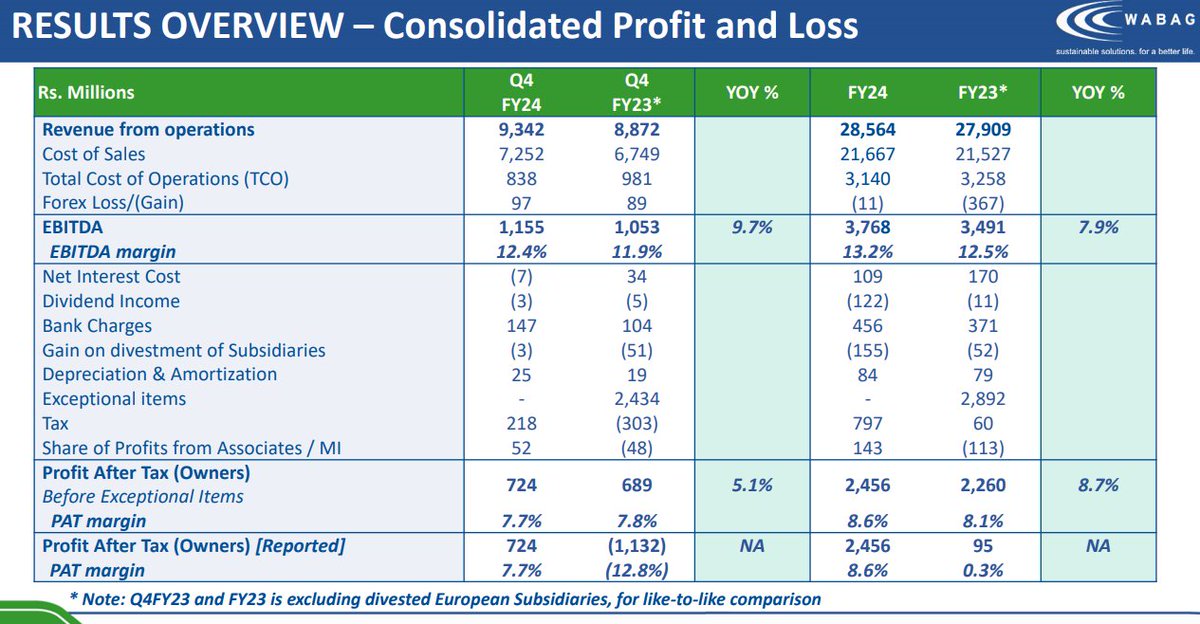

So how were the Q4FY24 results?

🥤Revenue grew at 9.7%

🥤Margins were at 12.4%

🥤Profit grew at 5.1%

Overall a steady set of numbers

🥤Revenue grew at 9.7%

🥤Margins were at 12.4%

🥤Profit grew at 5.1%

Overall a steady set of numbers

Order Book:-

🥤The order book is largely stable at INR11,448cr despite a slowdown in order intake in the domestic market due to the election code-of-conduct

🥤The management has guided at an order book of INR16,000cr for FY25. VATW has bid for orders worth ~USD1bn and is optimistic of order win

🥤 Entry into new segments (hydrogen fuel, biogas to CGB, and semiconductors) and markets (Middle East) will boost order inflow.

🥤The order book is largely stable at INR11,448cr despite a slowdown in order intake in the domestic market due to the election code-of-conduct

🥤The management has guided at an order book of INR16,000cr for FY25. VATW has bid for orders worth ~USD1bn and is optimistic of order win

🥤 Entry into new segments (hydrogen fuel, biogas to CGB, and semiconductors) and markets (Middle East) will boost order inflow.

Entry to natural gas thru Biogas:-

The company is going to convert biogas into natural gas

Government has fixed the tariff for that.

If you sell it to the government, even PSUs, gas stations where you go and fill this gas for your vehicles or you put it in the pipeline, which are running near your plant, you can have an agreement, a metering system where you can pump it into that. the rate they have fixed are very very attractive,

The company is going to convert biogas into natural gas

Government has fixed the tariff for that.

If you sell it to the government, even PSUs, gas stations where you go and fill this gas for your vehicles or you put it in the pipeline, which are running near your plant, you can have an agreement, a metering system where you can pump it into that. the rate they have fixed are very very attractive,

Future Guidance

🥤Visibility of a 15% to 20% growth on a 3 to 5 year basis

🥤Margins to remain in the region of 10-12%

🥤Expansion into the international market will be a key monitorable

🥤Expansion into Biogas and hydrogen will be a key monitorable

🥤Visibility of a 15% to 20% growth on a 3 to 5 year basis

🥤Margins to remain in the region of 10-12%

🥤Expansion into the international market will be a key monitorable

🥤Expansion into Biogas and hydrogen will be a key monitorable

🥤The management will continue to focus on the E&P projects rather than EPC projects.

🥤The management is targeting an order book of ₹16,000 crore in FY26E and has guided ~3x of revenue in the medium term and revenue mix of >50% International Projects, 30% Industrial Customers and 1/3rd of EPC being EP Projects.

🥤Focus on asset light model & working capital to improve ROCE:

🥤Geographical orderbook breakup: Domestic 69%, international 31%.

🥤The management is targeting an order book of ₹16,000 crore in FY26E and has guided ~3x of revenue in the medium term and revenue mix of >50% International Projects, 30% Industrial Customers and 1/3rd of EPC being EP Projects.

🥤Focus on asset light model & working capital to improve ROCE:

🥤Geographical orderbook breakup: Domestic 69%, international 31%.

Valuation:-

Va tech Vabag trades at 30x P/E multiple

This is certainly not cheap

Va tech Vabag trades at 30x P/E multiple

This is certainly not cheap

Conclusion

🥤Water recycling is a theme for the next 100 years

🥤Va tech Wabag is a market leader in the water purification space

🥤Given the asset light and patented technology it would be interesting to monitor the stock closely

🥤Water recycling is a theme for the next 100 years

🥤Va tech Wabag is a market leader in the water purification space

🥤Given the asset light and patented technology it would be interesting to monitor the stock closely

Keep following me -@AdityaD_Shah as I write daily to make you aware around:

📈Personal Finance

📈Investing

📈Stock Analysis

Go to my profile and hit the bell icon🔔to always stay updated

📈Personal Finance

📈Investing

📈Stock Analysis

Go to my profile and hit the bell icon🔔to always stay updated

Disclaimer:-

This is my own study.

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

This is my own study.

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

Loading suggestions...