5 statistical illusions that uncover why your backtests are misleading.

1. Data snooping.

1. Data snooping.

This occurs from overfitting a strategy to noise in the data by commonly testing too many parameters with your optimization.

Such as using 50 parameters on 2 years of data.

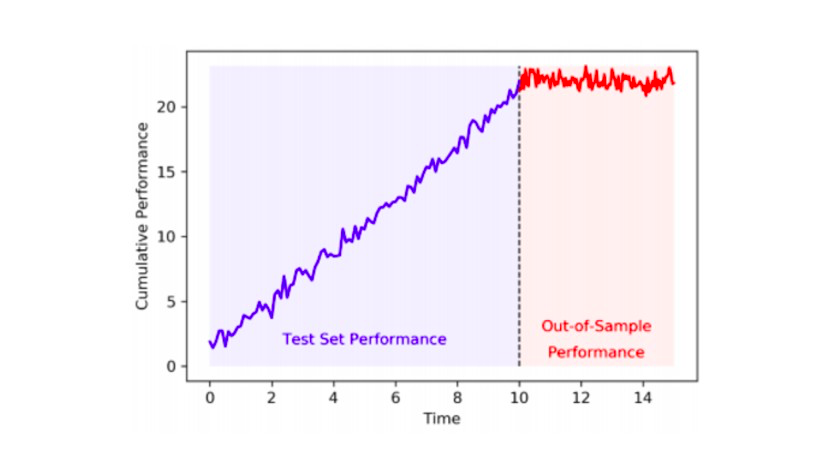

A good way to avoid this is to focus on simplicity, use out-of-sample testing and logical parameters.

Such as using 50 parameters on 2 years of data.

A good way to avoid this is to focus on simplicity, use out-of-sample testing and logical parameters.

2. Survivorship bias.

When you include only stocks or assets that are still trading, excluding those that have gone bankrupt or been delisted.

This can significantly alter backtest results by missing trades on stocks that have disappeared.

Always use point-in-time data.

When you include only stocks or assets that are still trading, excluding those that have gone bankrupt or been delisted.

This can significantly alter backtest results by missing trades on stocks that have disappeared.

Always use point-in-time data.

3. Cost underestimation.

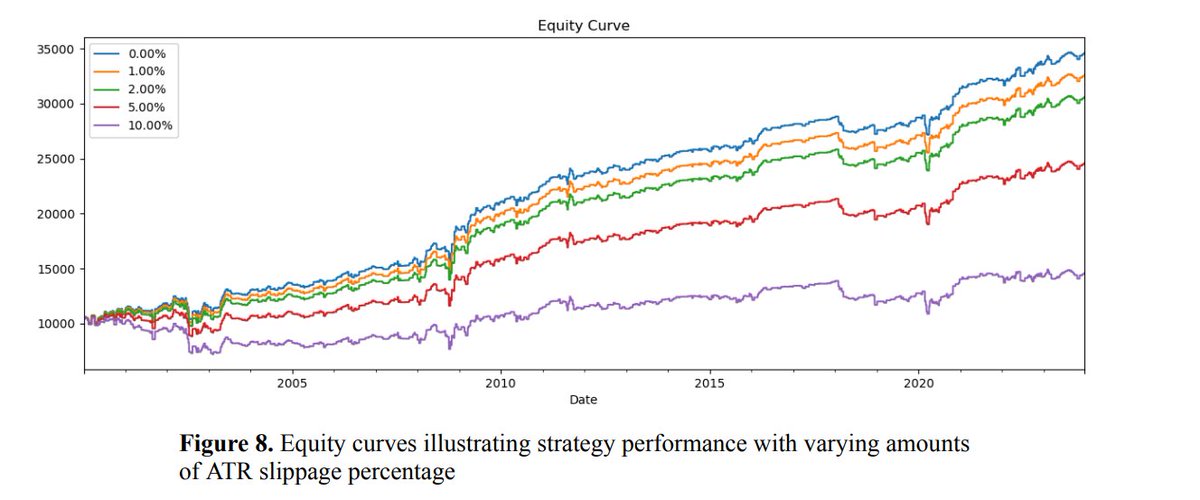

Many traders overlook realistic trading costs in their backtests.

This oversight is easy to fix, but it can be uncomfortable to reveal that numerous backtests turn unprofitable.

Always include commissions, slippage, spread, etc.

Many traders overlook realistic trading costs in their backtests.

This oversight is easy to fix, but it can be uncomfortable to reveal that numerous backtests turn unprofitable.

Always include commissions, slippage, spread, etc.

4. Look-ahead.

As Ernest Chan notes, this is a common programming mistake.

I've also seen traders make this error when using Excel to analyze data.

It happens when future information is used that wouldn't have been available at the time of the trade.

As Ernest Chan notes, this is a common programming mistake.

I've also seen traders make this error when using Excel to analyze data.

It happens when future information is used that wouldn't have been available at the time of the trade.

5. Time Period Bias.

This occurs when conclusions are based on insufficient or cherry-picked data, like backtesting an OTC long strategy only in 2020 and 2021.

Test strategies across multiple market cycles, ideally over five years plus, for statistically significant results.

This occurs when conclusions are based on insufficient or cherry-picked data, like backtesting an OTC long strategy only in 2020 and 2021.

Test strategies across multiple market cycles, ideally over five years plus, for statistically significant results.

If you find this type of content valuable & want more every week:

1. Follow me @GoshawkTrades for more.

2. Jump to the top & retweet.

1. Follow me @GoshawkTrades for more.

2. Jump to the top & retweet.

And If you want help to automate or backtest your strategy,

Book a call with me below:

unbiasedtrading.info

Book a call with me below:

unbiasedtrading.info

Loading suggestions...