1/18 To analyse the impact of Starlink on Econet Wireless Zimbabwe (EWZ) we first need a recap of the telecommunications (telco) business model in its simplest form.

Let's unpack this and then later how Starlink comes in.

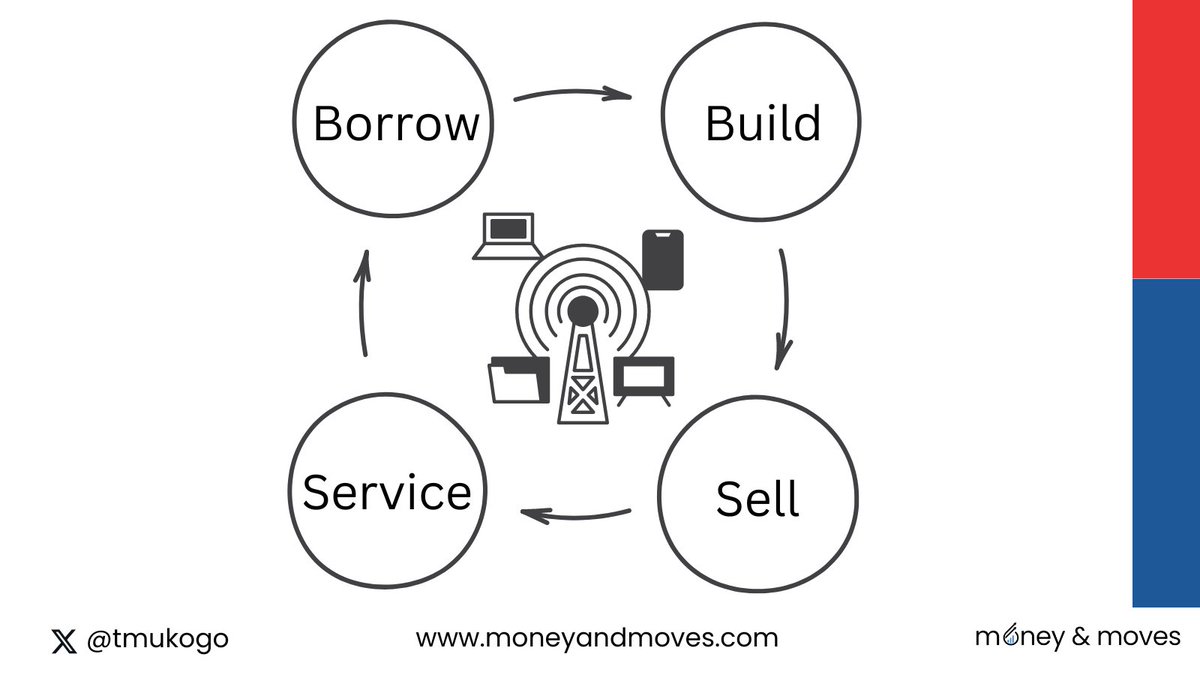

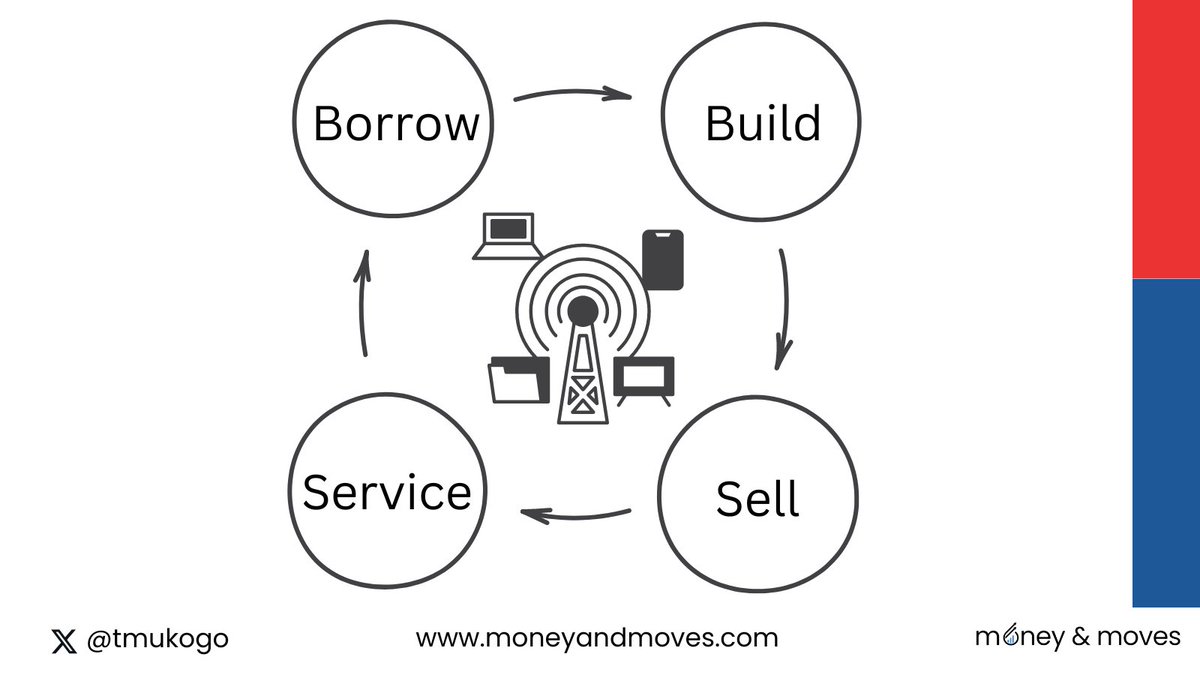

The telco business model is made up of four key sequential, simultaneous, and repeating cycles.

🏦 Borrow 🛰️ Build 🤳 Sell 🤝 Service.

This is a simplification but let me explain each cycle and then illustrate with MTN.

Let's unpack this and then later how Starlink comes in.

The telco business model is made up of four key sequential, simultaneous, and repeating cycles.

🏦 Borrow 🛰️ Build 🤳 Sell 🤝 Service.

This is a simplification but let me explain each cycle and then illustrate with MTN.

2/18 The first thing telcos need to do is BORROW because telecoms is a capital-intensive business and so self-funding is difficult.

Once you've borrowed, you BUILD (and maintain) the network and infrastructure that people will use (think base stations, etc.).

After that, you SELL people access to the network so they can make calls and use data etc. and with the sales you generate profits.

Then, with those profits, you SERVICE the loans (i.e., pay back the banks) and since you've serviced the loans, you can then BORROW more money, and the cycle repeats.

Once you've borrowed, you BUILD (and maintain) the network and infrastructure that people will use (think base stations, etc.).

After that, you SELL people access to the network so they can make calls and use data etc. and with the sales you generate profits.

Then, with those profits, you SERVICE the loans (i.e., pay back the banks) and since you've serviced the loans, you can then BORROW more money, and the cycle repeats.

3/18 🏦 Borrow 🛰️ Build 🤳 Sell 🤝 Service 🔂

As long as all four cycles work well, you can repeat this continuously and make loads of money.

Let's look at MTN's financial statements for a concrete illustration.

As long as all four cycles work well, you can repeat this continuously and make loads of money.

Let's look at MTN's financial statements for a concrete illustration.

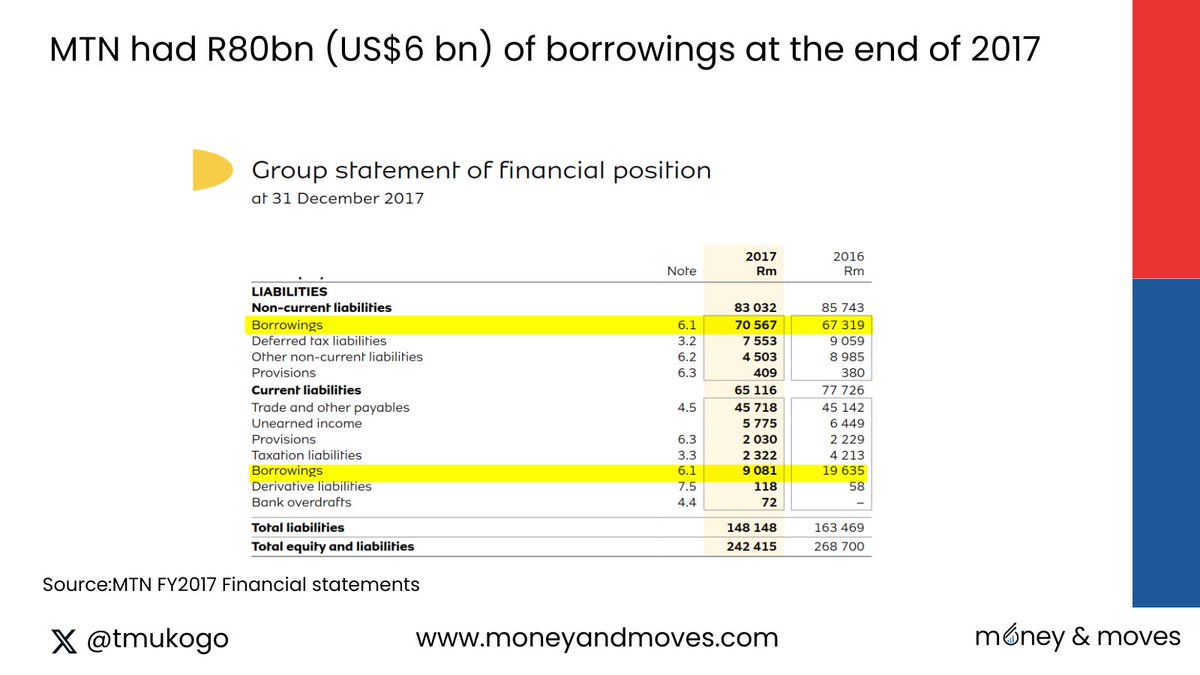

4/18 Starting with 2017, MTN had R80 billion in BORROWINGS by the end of their financial year.

As one of South Africa's biggest companies, MTN generally can raise capital.

As one of South Africa's biggest companies, MTN generally can raise capital.

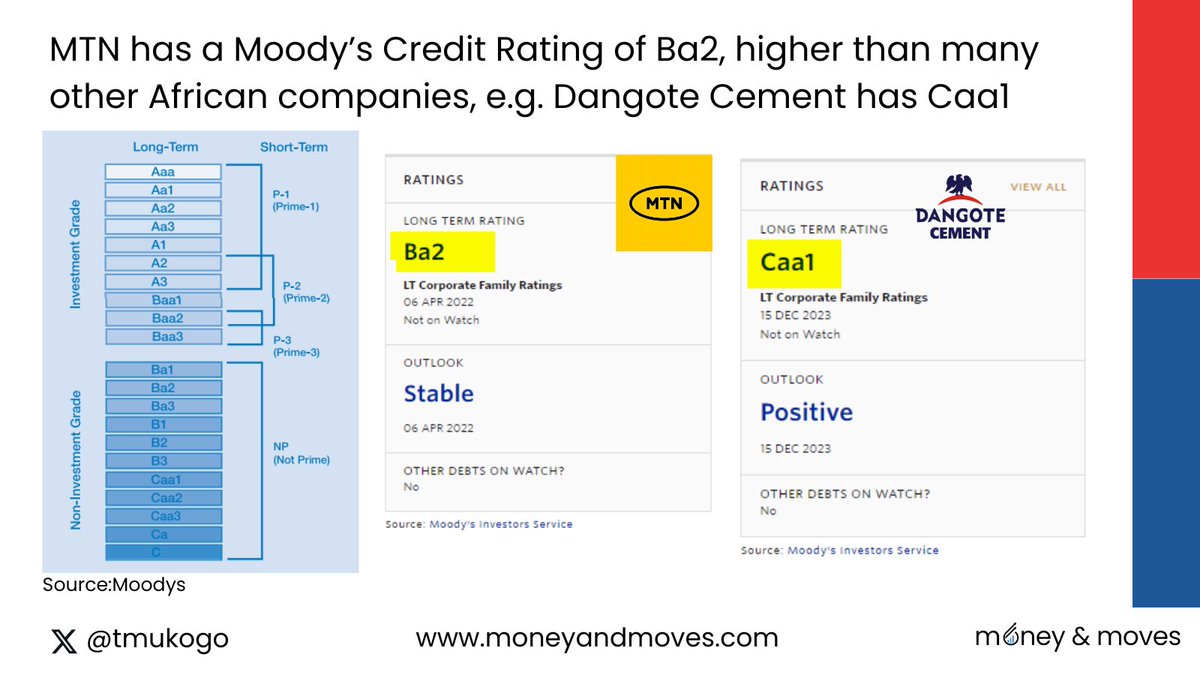

5/18 They also have a higher credit rating than most African companies which helps.

For example, MTN has a credit rating of Ba2 rating from Moody's, while Dangote Cement has a much lower rating at Caa1.

Borrow: ✅

For example, MTN has a credit rating of Ba2 rating from Moody's, while Dangote Cement has a much lower rating at Caa1.

Borrow: ✅

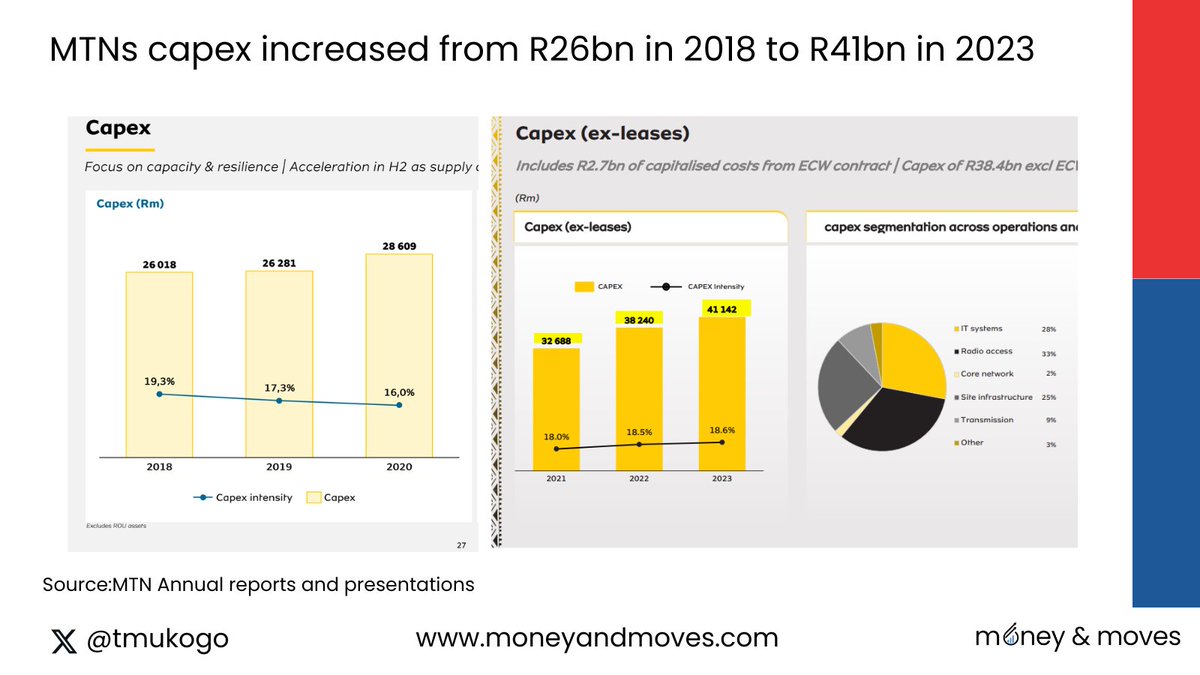

6/18 MTN used this capital raised to BUILD and maintain their network, as shown by their gradually increasing capital expenditure (CAPEX) from R26 billion in 2018 to R41 billion in 2023.

Build: ✅

Build: ✅

7/18 With the network in place and working well, MTN was able to sell more services every year as is shown by the 11% annual revenue growth between 2018-22.

This in turn led to an increase in return on equity (a measure of profitability) which nearly doubled.

Sell: ✅

This in turn led to an increase in return on equity (a measure of profitability) which nearly doubled.

Sell: ✅

8/18 With the profits, MTN SERVICED its loans, as seen in the gradual decrease in net debt which went from R55bn in 2019 down to R32bn in 2023.

You also see this in their cashflow statements where they regularly pay back loans and and then get more funding.

Service:✅

You also see this in their cashflow statements where they regularly pay back loans and and then get more funding.

Service:✅

9/18 In reality, all these steps happen both sequentially and simultaneously.

You're borrowing money, building your network, selling services, and servicing loans at the same time.

When everything works, it's a beautiful and profitable business model.

You're borrowing money, building your network, selling services, and servicing loans at the same time.

When everything works, it's a beautiful and profitable business model.

10/18 Now with the emergence of Starlink the "Sell" cycle for telcos like Econet Wireless Zimbabwe (EWZ) will be impacted as Starlink may eat into data revenues.

But this disruption also depends on how much revenue EWZ gets from data.

The below shows that in 2023 about 33% of EWZ's revenue was from data.

Compared to the regional peers EWZ actually had a lower share of revenue from data than others.

This data suggests that EWZ's share of data revenue has room to grow to be closer to peers especially with better pricing.

But this disruption also depends on how much revenue EWZ gets from data.

The below shows that in 2023 about 33% of EWZ's revenue was from data.

Compared to the regional peers EWZ actually had a lower share of revenue from data than others.

This data suggests that EWZ's share of data revenue has room to grow to be closer to peers especially with better pricing.

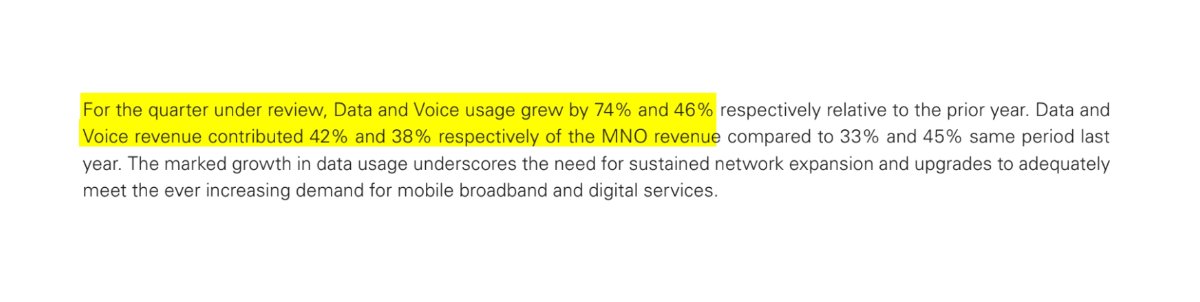

11/18 We may have already seen this happening.

In EWZ's most recent quarter (March - May) we saw the share of data revenue increaseby 74% to get to a total of 42% of Mobile Network revenues.

In EWZ's most recent quarter (March - May) we saw the share of data revenue increaseby 74% to get to a total of 42% of Mobile Network revenues.

12/18 So with Starlink coming in, it will certainly eat into some of EWZ's customer base, but I think overall there will be an increase in data revenue as more people use packages like the Smart Biz package, which fits most users' needs.

So margins on data will be lower due to pricing competition but the increase in volumes may mean the business is not too badly affected.

This makes sense sense Starlink is not exactly a direct replacement for mobile data.

So margins on data will be lower due to pricing competition but the increase in volumes may mean the business is not too badly affected.

This makes sense sense Starlink is not exactly a direct replacement for mobile data.

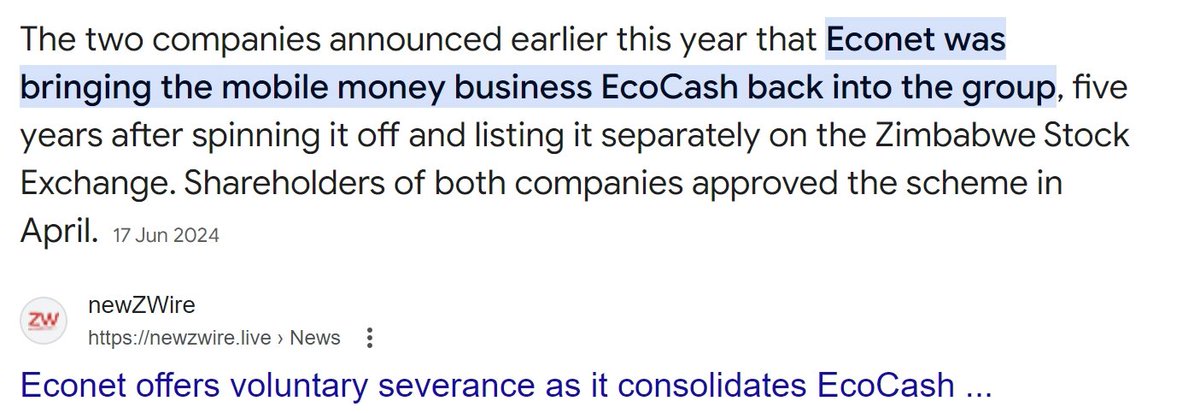

13/18 I think for EWZ, Innbucks and similar players probably pose a greater threat than Starlink, as mobile financial services are really the most valuable growth opportunity in telecoms.

This explains why EWZ made the decision to bring back EcoCash.

This explains why EWZ made the decision to bring back EcoCash.

14/18 This is not to say EWZ is celebrating the entry of Starlink.

As shown earlier data revenue was a growing source of revenue and so they would have preferred to have less competition.

Without Starlink that $45 Smart Biz package could have easily been $55 and had uptake.

But on short Starlink won't kill EWZ. Starlink isn't the biggest risk EWZ is facing.

The business that is most affected by Starlink is probably Liquid Intelligent Technologies, more commonly just known as Liquid.

As shown earlier data revenue was a growing source of revenue and so they would have preferred to have less competition.

Without Starlink that $45 Smart Biz package could have easily been $55 and had uptake.

But on short Starlink won't kill EWZ. Starlink isn't the biggest risk EWZ is facing.

The business that is most affected by Starlink is probably Liquid Intelligent Technologies, more commonly just known as Liquid.

15/18 Now I know some people are thinking that Liquid is the same as Econet Wireless Zimbabwe (EWZ) so let's unpack the relationship.

Both Econet Wireless Zimbabwe and Liquid are part of the same group, Econet Wireless Global.

However, EWZ and Liquid are two separate businesses.

EWZ is the telco business (the cellphone network people), whereas Liquid is the internet infrastructure business (the fiber network and related services people).

They have separate management teams and separate P&Ls.

Both Econet Wireless Zimbabwe and Liquid are part of the same group, Econet Wireless Global.

However, EWZ and Liquid are two separate businesses.

EWZ is the telco business (the cellphone network people), whereas Liquid is the internet infrastructure business (the fiber network and related services people).

They have separate management teams and separate P&Ls.

16/18 Perhaps why the two businesses are confused is that EWZ still owns a stake in Liquid and EWZ is still a big customer of Liquid, which sells data to them which they sell to end customers.

So when I say EWZ should be fine its referring to the Mobile Network business.

This statement doesn't apply in the same way to Liquid

Liquid will likely be significantly impacted by Starlink.

So when I say EWZ should be fine its referring to the Mobile Network business.

This statement doesn't apply in the same way to Liquid

Liquid will likely be significantly impacted by Starlink.

17/18 We will need to unpack just how much in a follow up thread or a post on the email list.

So make sure you follow me @tmukogo and set notification on and also join the free email list (link in Bio).

Let me know what do you think. Do you agree? Leave a comment!

I am working with public information and so I could be wrong or missing something in my analysis. If so please let me know!

So make sure you follow me @tmukogo and set notification on and also join the free email list (link in Bio).

Let me know what do you think. Do you agree? Leave a comment!

I am working with public information and so I could be wrong or missing something in my analysis. If so please let me know!

18/18 Thanks for reading!

I write on the finance and strategy behind the companies you care about the most. Follow me @tmukogo for more.

Please comment on / repost the below tweet! I would love to get your feedback!

I write on the finance and strategy behind the companies you care about the most. Follow me @tmukogo for more.

Please comment on / repost the below tweet! I would love to get your feedback!

Loading suggestions...