The book "Capital Returns" offers a powerful framework for investing successfully.

In this thread, I explain the capital cycle, Marathon's core investment framework, and four main key takeaways.

Let's dive in!

In this thread, I explain the capital cycle, Marathon's core investment framework, and four main key takeaways.

Let's dive in!

What is the capital cycle?

1. New capital is attracted into sectors with outsized profits

2. Eventually, this influx of capital causes supply to overshoot

3. Weaker firms exit and capital leaves the industry

4. As a result, returns on capital for remaining firms increase

1. New capital is attracted into sectors with outsized profits

2. Eventually, this influx of capital causes supply to overshoot

3. Weaker firms exit and capital leaves the industry

4. As a result, returns on capital for remaining firms increase

By focusing on the supply side (competitors spending less) rather than the demand side (customers spending more), we can gain an edge when investing.

The core framework is that companies in industries with a benign supply side can maintain higher profitability for longer.

The core framework is that companies in industries with a benign supply side can maintain higher profitability for longer.

There are 4 main takeaways that can help improve our investing:

1. Companies with strong moats can maintain profitability for longer than the market expects

Some companies have such strong competitive advantages that they can prevent supply from entering the market. This allows them to maintain profits (e.g. through pricing power)

Some companies have such strong competitive advantages that they can prevent supply from entering the market. This allows them to maintain profits (e.g. through pricing power)

Pricing power can come from concentrated market structure and/or intrinsic pricing power. This could be cases where the cost is a small portion of the total bill, when switching costs are high, technology leadership, etc. Eg. $TDG

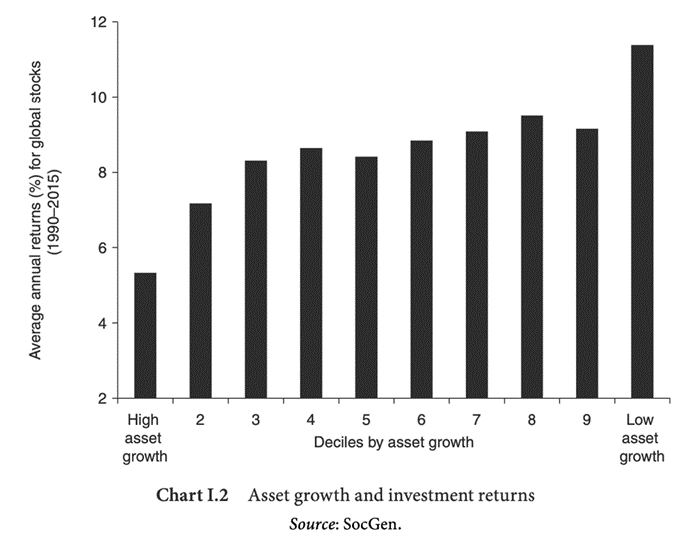

2. Firms with lower asset growth outperform

Asset expansion — such as M&A, equity issuance, and new loans — tends to be followed by low returns.

Asset contraction — such as spin-offs, share repurchases, or debt paydown — tends to be followed by positive excess returns.

Asset expansion — such as M&A, equity issuance, and new loans — tends to be followed by low returns.

Asset contraction — such as spin-offs, share repurchases, or debt paydown — tends to be followed by positive excess returns.

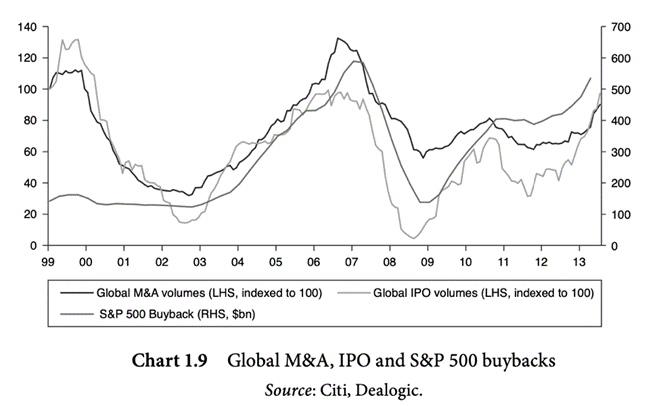

Bankers with short time horizons accelerate this process by encouraging large numbers of IPOs and M&A late in the cycle to maximize fees.

This is why most IPOs tend to underperform, as they happen near the tops of cycles and thus have high starting valuations.

This is why most IPOs tend to underperform, as they happen near the tops of cycles and thus have high starting valuations.

3. Cyclical companies look cheap at the top and expensive at the bottom

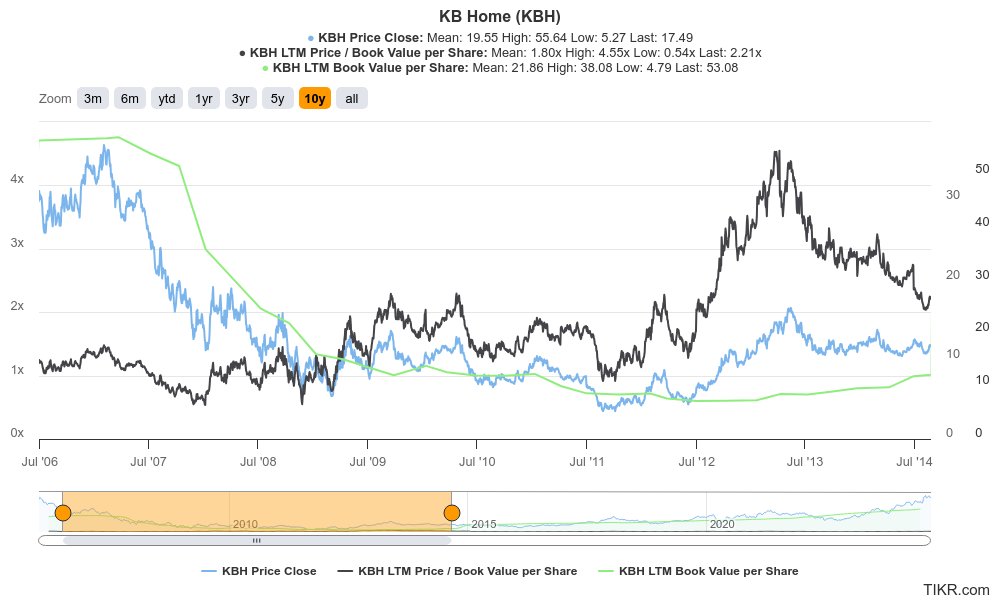

US homebuilders grew their assets rapidly leading up to home prices peaking in 2006. Investors who bought near the end of the cycle when they were trading around book value ended up with significant losses.

US homebuilders grew their assets rapidly leading up to home prices peaking in 2006. Investors who bought near the end of the cycle when they were trading around book value ended up with significant losses.

For example, KB Home grew rapidly between 2001 and 2006.

By the summer of 2006, its shares were trading at an optically cheap valuation of 1.2x book.

From that point, KB’s book value declined by 85%, and its shares fell a further 75%.

By the summer of 2006, its shares were trading at an optically cheap valuation of 1.2x book.

From that point, KB’s book value declined by 85%, and its shares fell a further 75%.

Counterintuitively, the best time to buy cyclicals may be when they are trading at a high P/E multiple on depressed earnings at the bottom of a cycle.

4. Strong management allocates capital in a counter-cyclical manner

Buffett once said: "After ten years on the job, a CEO whose company retains 10% of earnings will have been responsible for the deployment of more than 60% of all capital at work in the business"

Buffett once said: "After ten years on the job, a CEO whose company retains 10% of earnings will have been responsible for the deployment of more than 60% of all capital at work in the business"

Managers frequently confuse a benign cycle with skill and overinvest, especially as they feel pressure not to lose market share.

Similarly in investing, everyone looks like a genius in a bull market, but that may just be due to excessive risk-taking rather than true skill.

Similarly in investing, everyone looks like a genius in a bull market, but that may just be due to excessive risk-taking rather than true skill.

Good management allocates capital in a counter-cyclical manner and is properly incentivized.

They are dispassionate about selling assets when someone is willing to overpay in a bull market, and are prepared to acquire from distressed sellers in a recession.

They are dispassionate about selling assets when someone is willing to overpay in a bull market, and are prepared to acquire from distressed sellers in a recession.

TLDR:

1. Companies with strong moats can maintain profitability for longer than expected

2. Firms with lower asset growth outperform

3. Cyclical companies look cheap at the top and expensive at the bottom

4. Strong management allocates capital in a counter-cyclical manner

1. Companies with strong moats can maintain profitability for longer than expected

2. Firms with lower asset growth outperform

3. Cyclical companies look cheap at the top and expensive at the bottom

4. Strong management allocates capital in a counter-cyclical manner

Applying these lessons, Marathon likes two types of investments:

1. Cyclicals where supply is declining, leading to attractive valuations

2. Quality businesses with strong moats that allow them to earn high returns on capital

1. Cyclicals where supply is declining, leading to attractive valuations

2. Quality businesses with strong moats that allow them to earn high returns on capital

Thanks for reading!

If you enjoyed the thread, it would mean a lot if you could like and repost it.

I quit my job at a hedge fund and left Wall Street to help level the playing field for individual investors.

If you’d like to learn how to invest, check out Superinvesting.

If you enjoyed the thread, it would mean a lot if you could like and repost it.

I quit my job at a hedge fund and left Wall Street to help level the playing field for individual investors.

If you’d like to learn how to invest, check out Superinvesting.

Loading suggestions...