The Indian CDMO Playbook🧵

This is a fairly long thread (30-45 mins) but promise it'll be worth it as it contains the distillation of my entire CDMO sector study.

Kindly Repost if this adds value

This is a fairly long thread (30-45 mins) but promise it'll be worth it as it contains the distillation of my entire CDMO sector study.

Kindly Repost if this adds value

Part 1: The Basics

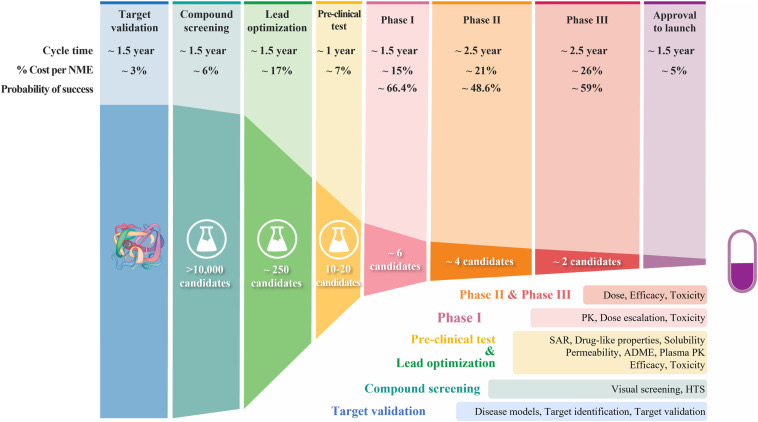

Before diving into the sector, let’s first understand why CDMOs exist. For that, we need to know how novel drugs (for diseases without existing therapies) are discovered and developed.

Before diving into the sector, let’s first understand why CDMOs exist. For that, we need to know how novel drugs (for diseases without existing therapies) are discovered and developed.

Three things to know about novel drugs:

1. It takes 12-15 years to discover a new therapy.

2. Average cost is USD 1-2 bn. (>USD 2.5bn+ for some therapies in oncology and immunology).

3. Only 1 compound gets approved out of 5-10 thousand compounds.

1. It takes 12-15 years to discover a new therapy.

2. Average cost is USD 1-2 bn. (>USD 2.5bn+ for some therapies in oncology and immunology).

3. Only 1 compound gets approved out of 5-10 thousand compounds.

Bottom line: It’s incredibly time-consuming and costly to make novel drugs. However, 20% of patented drugs command 80% of the market by value. So, it’s a high-risk-reward proposition for pharma companies. This creates the following pain areas:

1. The total patent period is 20 years, leaving 7-12 years for monetization

2. Companies need to be cost-efficient else risk-reward goes for a toss

3. Stringent criteria for regulatory submissions

4. Post-regulatory exclusivity, generic players create pricing pressure

2. Companies need to be cost-efficient else risk-reward goes for a toss

3. Stringent criteria for regulatory submissions

4. Post-regulatory exclusivity, generic players create pricing pressure

Part 2: The Value Proposition

A typical CDMO handles an end-to-end mfg. supply chain for the pharma company, from sourcing raw materials to drug development on a clinical scale and manufacturing on a commercial scale.

This value chain graphic will give you a better idea.

A typical CDMO handles an end-to-end mfg. supply chain for the pharma company, from sourcing raw materials to drug development on a clinical scale and manufacturing on a commercial scale.

This value chain graphic will give you a better idea.

But what are the benefits of outsourced manufacturing?

The answer lies in four Cs:

The answer lies in four Cs:

1. Cost: Economies of scale lead to cost efficiencies. CDMOs offer 35-70% reduction in operating costs. CDMOs help variablize the cost structure.

2. Capabilities: CDMOs constantly invest in new drug modalities like ADC, peptides, mAbs, cell and gene therapies.

2. Capabilities: CDMOs constantly invest in new drug modalities like ADC, peptides, mAbs, cell and gene therapies.

3. Core focus: Pharma companies can focus on research, building a drug development pipeline, and improving physician outreach.

4. Capital light: Manufacturing is capital intensive. With CDMOs, the model shifts from capex-centric to opex-centric.

4. Capital light: Manufacturing is capital intensive. With CDMOs, the model shifts from capex-centric to opex-centric.

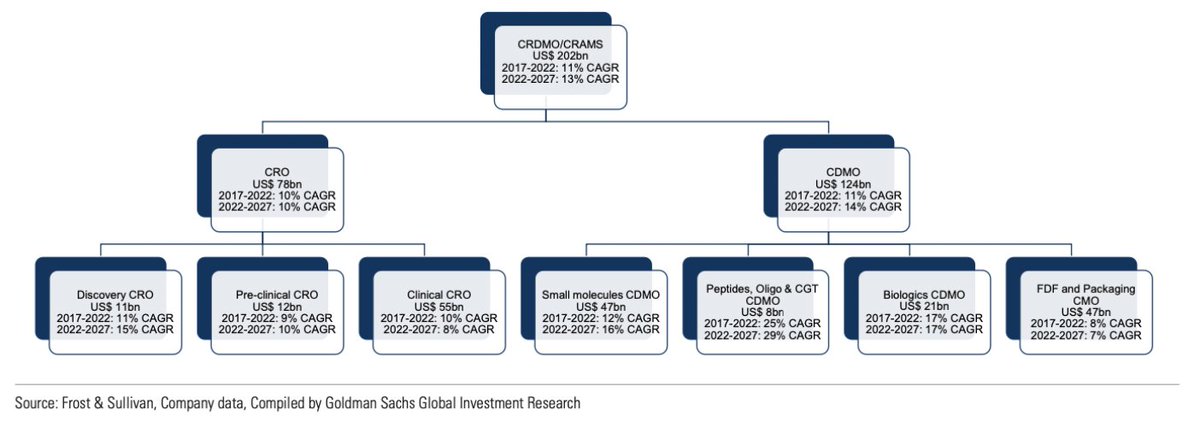

Part 3: The Value Migration

The CDMO market has grown at a CAGR of 10% vis-a-vis the global pharma market CAGR of 5-6% over the last decade. The momentum will continue with new drug modalities driving higher outsourcing.

The CDMO market has grown at a CAGR of 10% vis-a-vis the global pharma market CAGR of 5-6% over the last decade. The momentum will continue with new drug modalities driving higher outsourcing.

Part 4: The India Advantage

Over the last decade, APAC-based CDMOs including Wuxi AppTec and Samsung Biologics have grown exponentially owing to higher cost savings in this region.

However, with the Biosecure Act, innovators are looking to diversify supply chains.

Over the last decade, APAC-based CDMOs including Wuxi AppTec and Samsung Biologics have grown exponentially owing to higher cost savings in this region.

However, with the Biosecure Act, innovators are looking to diversify supply chains.

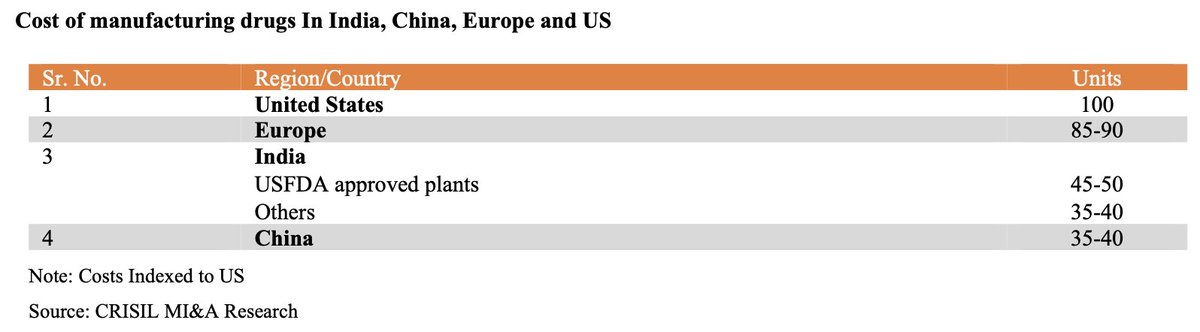

Structurally, India offers a few advantages due to its unique characteristics. Here are the key ones.

1. Talent pool: Abundant supply of STEM talent at cost-effective rates.

2. Cost-efficiencies: Building in India is cost-effective.

1. Talent pool: Abundant supply of STEM talent at cost-effective rates.

2. Cost-efficiencies: Building in India is cost-effective.

3. Eco-system: Mature pharma infrastructure with 3,000 manufacturers and 10,500 facilities. Also, with FDI and PLI, policy support enhances overall appeal.

4. Capabilities: Indian CDMOs like Syngene, Suven, and Piramal Pharma are investing in cutting-edge modalities.

4. Capabilities: Indian CDMOs like Syngene, Suven, and Piramal Pharma are investing in cutting-edge modalities.

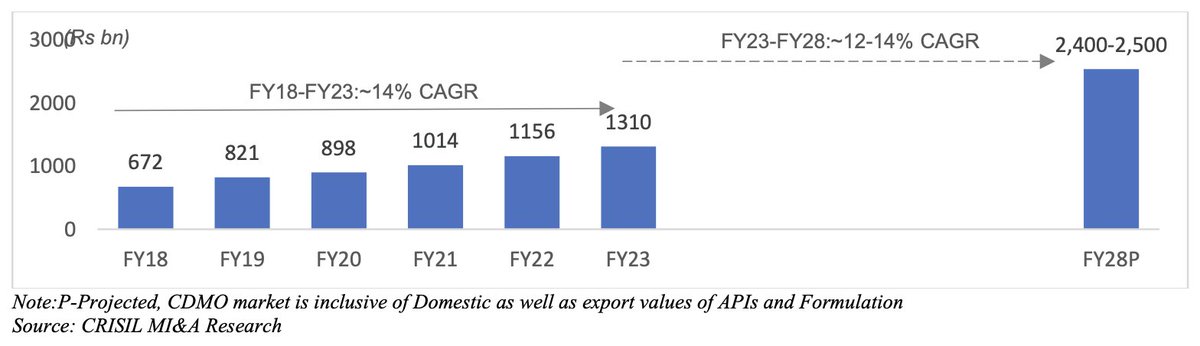

Part 5: The Domestic CDMO Opportunity

Indian CDMOs serve both innovators and generic pharma. While the global opportunity is larger, outsourcing is also picking up in the domestic pharma market.

Indian CDMOs serve both innovators and generic pharma. While the global opportunity is larger, outsourcing is also picking up in the domestic pharma market.

Outsourcing penetration in IPM is expected to increase from 30-35% in FY23 to 40-45% in FY28. Generic-focused CDMOs are expected to grow faster than IPM.

But why are Indian Generic Pharma players outsourcing despite having scale and low-cost advantage?

Here are some of the key trends shaping this industry.

Here are some of the key trends shaping this industry.

1) Broader shift in perception: CDMOs now have complex dosage form capabilities and compliant infrastructure. Thus, there is growing confidence among Indian pharma companies with respect to quality that CDMOs offer.

2) Raising the bar: Indian CDMOs are constantly raising the bar with the capability additions in terms of various dosage forms. This allows Indian pharma companies to expand their portfolio faster than in-house development.

3) Moving up the value chain: Indian pharma players have increased R&D spending over the last decade and the focus of R&D is shifting from ANDA filings to developing novel medicines.

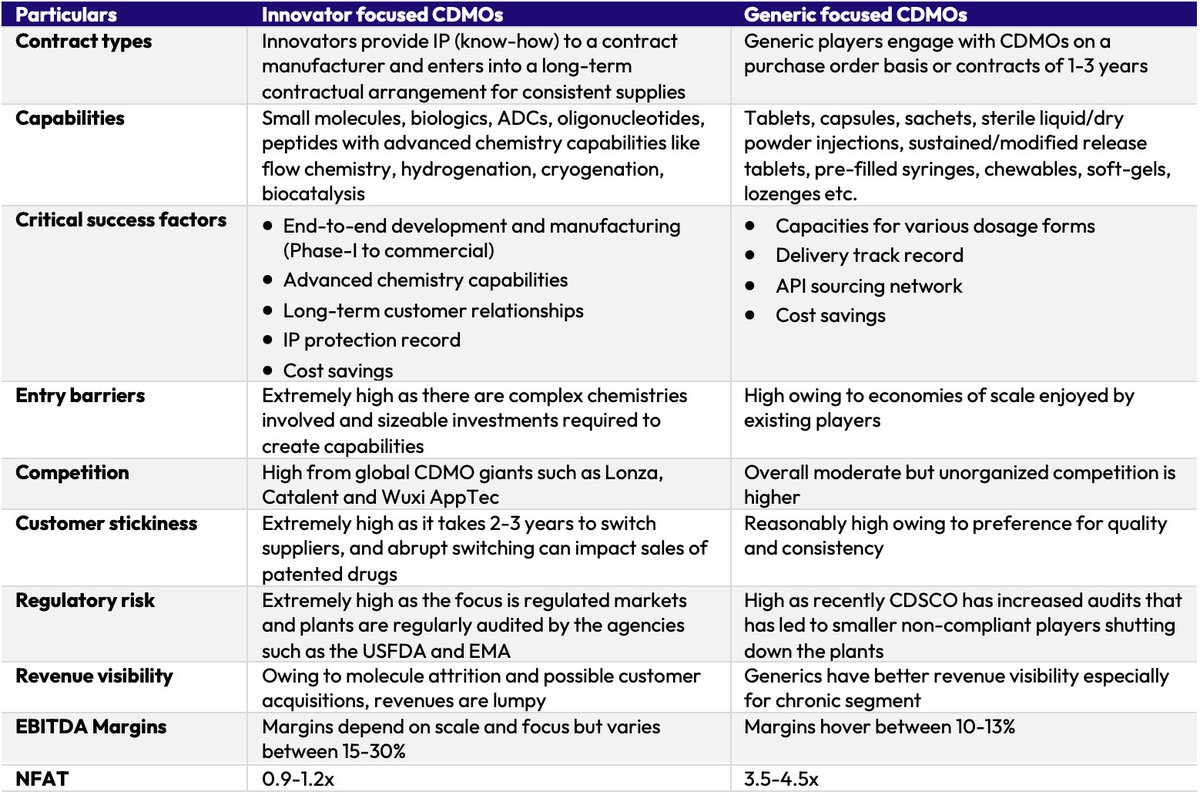

Part 6: The Comparative Economics

Here's a brief comparison between innovator and generic-focused business models in CDMO. To summarize, the innovator-focused model is about higher value addition and generic generic-focused model is about efficiency.

Here's a brief comparison between innovator and generic-focused business models in CDMO. To summarize, the innovator-focused model is about higher value addition and generic generic-focused model is about efficiency.

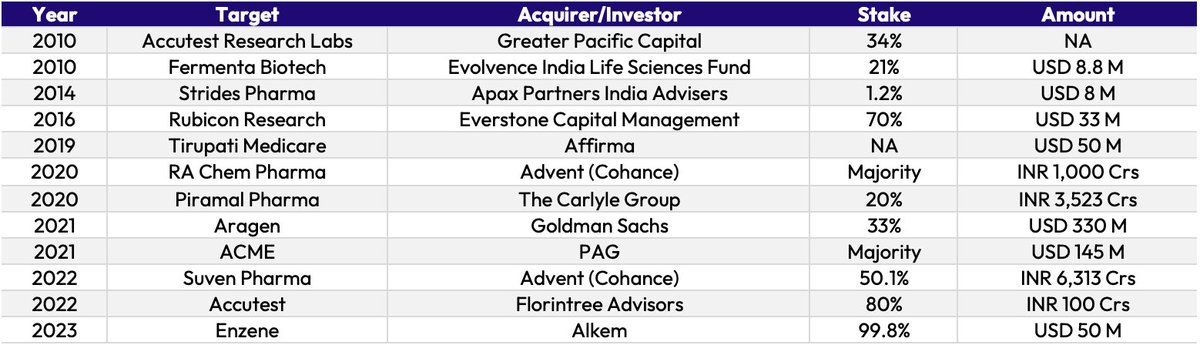

Part 7: The Capital Flow

Capital is chasing the sector which is evident from the recent PE deals as well as IPOs. Here's a snapshot of the same.

Capital is chasing the sector which is evident from the recent PE deals as well as IPOs. Here's a snapshot of the same.

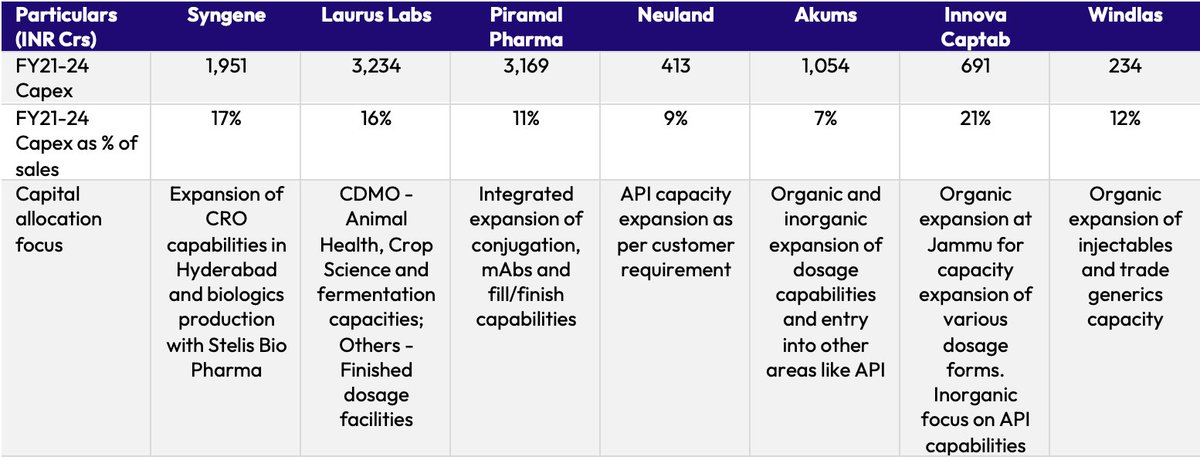

Part 8: The Capital Allocation

CDMOs are investing heavily in capacity/capability expansion. Innovator-focused peers are investing in complex chemistry capabilities, while domestic-focused peers are investing in dosage capacities and diversification to other areas such as API.

CDMOs are investing heavily in capacity/capability expansion. Innovator-focused peers are investing in complex chemistry capabilities, while domestic-focused peers are investing in dosage capacities and diversification to other areas such as API.

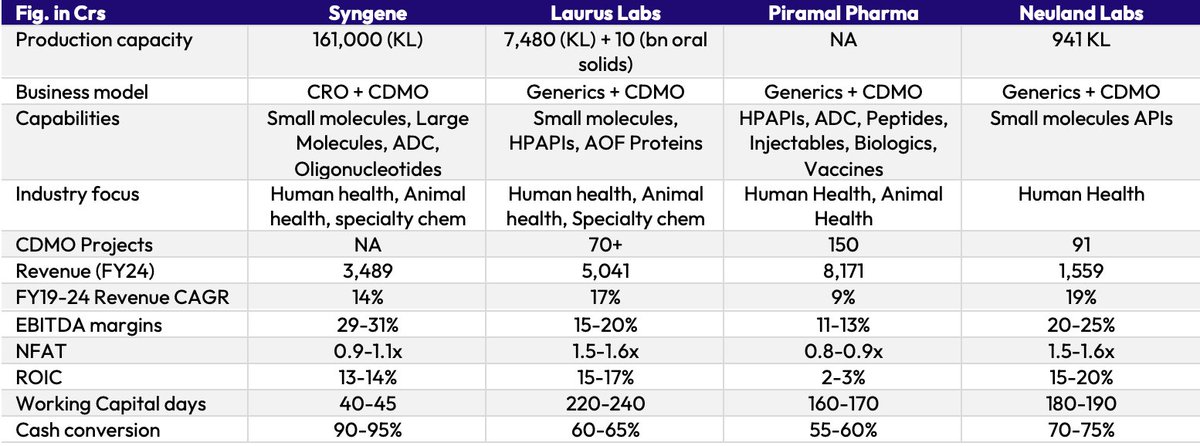

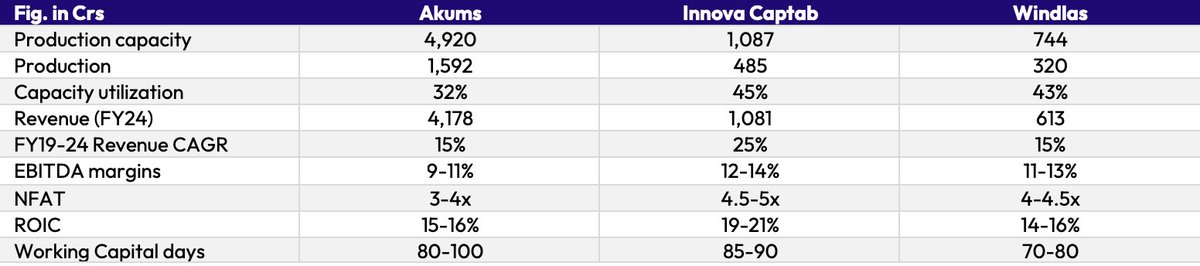

Part 9: The P2P Comparison

A sector analysis is incomplete without a P2P comparison. Here it is.

A sector analysis is incomplete without a P2P comparison. Here it is.

The Conclusion

Indian CDMO story has just started and we will soon see USD 1 bn+ peers. While @unseenvalue sir has covered innovator CDMOs in great detail, generic-focused CDMOs will likely throw in a positive surprise.

Indian CDMO story has just started and we will soon see USD 1 bn+ peers. While @unseenvalue sir has covered innovator CDMOs in great detail, generic-focused CDMOs will likely throw in a positive surprise.

Lastly, we provide quality equity research services to DIY investors in Indian markets. Here's where you can subscribe to our research.

exponentialresearch.in

exponentialresearch.in

Disc: No reco. Study is for educational purpose only.

Loading suggestions...