Vishal Mega Mart’s ₹8,000 crore IPO is here.

The retailer lags behind its rival DMart in profits. But it’s growing faster & has more stores.

However, this IPO has ONE BIG concern & many investors may not like it (Refer to Tweet 9).

Let’s dive into the details. A🧵

(1/15)

The retailer lags behind its rival DMart in profits. But it’s growing faster & has more stores.

However, this IPO has ONE BIG concern & many investors may not like it (Refer to Tweet 9).

Let’s dive into the details. A🧵

(1/15)

We will cover 5 key aspects in this analysis:

- Vishal Mega Mart’s business model

- Financials and valuations

- Compare its numbers with Avenue Supermarts

(DMart)

- Key IPO details

- Strengths and challenges

Let’s start. 👇

(2/15)

- Vishal Mega Mart’s business model

- Financials and valuations

- Compare its numbers with Avenue Supermarts

(DMart)

- Key IPO details

- Strengths and challenges

Let’s start. 👇

(2/15)

1. Business Model

Vishal Mega Mart targets middle-class consumers with a diverse portfolio:

-Apparel: 45% of revenue

-General merchandise: 28%

-FMCG goods: 27%

Over 70% of its revenue comes from in-house brands. This boosts its margins and reduces dependence on third-party products.

(3/15)

Vishal Mega Mart targets middle-class consumers with a diverse portfolio:

-Apparel: 45% of revenue

-General merchandise: 28%

-FMCG goods: 27%

Over 70% of its revenue comes from in-house brands. This boosts its margins and reduces dependence on third-party products.

(3/15)

With 645 stores across 414 cities (as of Sept 2024), Vishal Mega Mart is primarily a brick-and-mortar player.

Its online sales remain small, making up just 1% of traded goods revenue in the first half of FY25.

(4/15)

Its online sales remain small, making up just 1% of traded goods revenue in the first half of FY25.

(4/15)

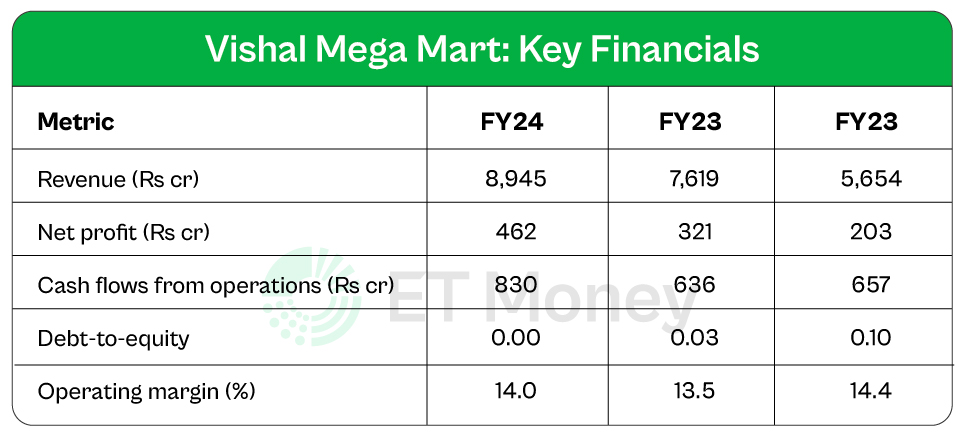

2. Financials & Valuations

The company's key financial metrics appear quite attractive.

In the last two years, its revenue has grown at 26% p.a.

Profits grew even faster at 51% annually.

Also, the company is debt-free & boasts strong operational cash flows.

(5/15)

The company's key financial metrics appear quite attractive.

In the last two years, its revenue has grown at 26% p.a.

Profits grew even faster at 51% annually.

Also, the company is debt-free & boasts strong operational cash flows.

(5/15)

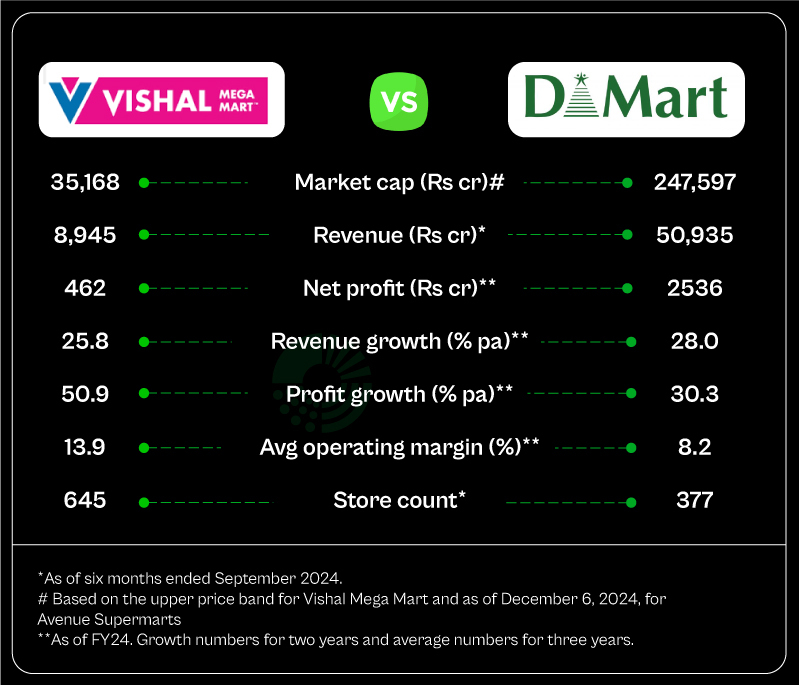

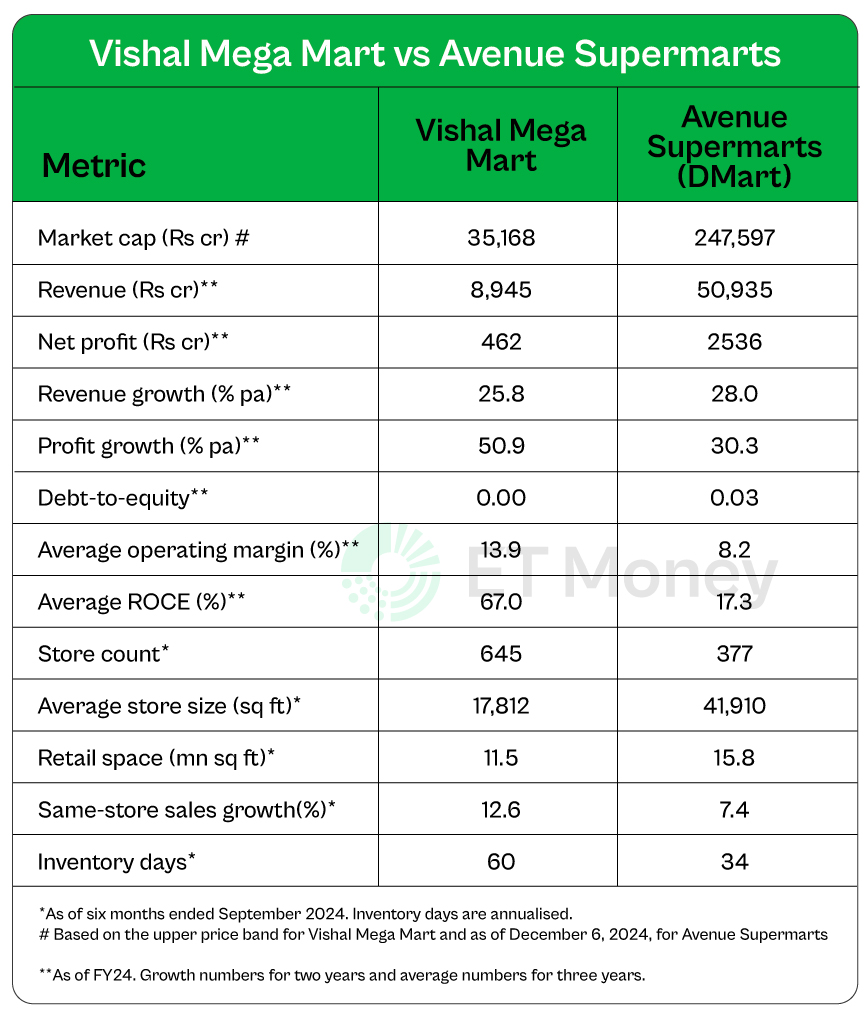

3. Comparison with DMart

Vishal runs 645 stores versus DMart’s 377.

But DMart’s stores are over twice as large, giving it 38% more retail space.

Vishal leads in same-store sales growth, but DMart sells inventory faster.

(6/15)

Vishal runs 645 stores versus DMart’s 377.

But DMart’s stores are over twice as large, giving it 38% more retail space.

Vishal leads in same-store sales growth, but DMart sells inventory faster.

(6/15)

DMart generates nearly 6x the revenue and 5x the profit of Vishal Mega Mart.

However, Vishal excels in terms of profit and revenue growth.

Vishal also has better operating margins.

Both companies are debt-free.

(7/15) x.com

However, Vishal excels in terms of profit and revenue growth.

Vishal also has better operating margins.

Both companies are debt-free.

(7/15) x.com

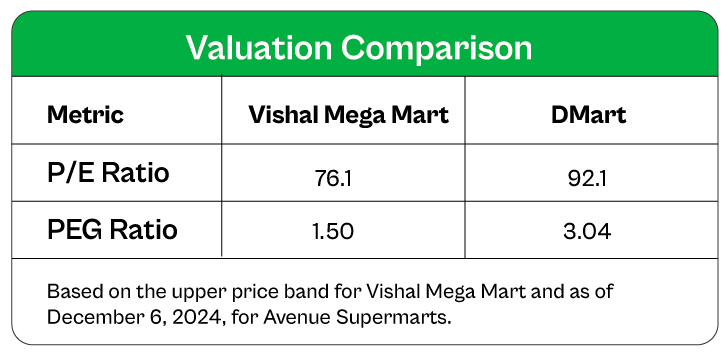

Now, let’s compare valuations.

In terms of the P/E, Vishal looks relatively more attractive.

Even the PEG ratio shows Vishal Mega Mart is fairly valued compared to DMart.

Overall, Vishal matches DMart quite well, and its valuations are the icing on the cake.

(8/15) x.com

In terms of the P/E, Vishal looks relatively more attractive.

Even the PEG ratio shows Vishal Mega Mart is fairly valued compared to DMart.

Overall, Vishal matches DMart quite well, and its valuations are the icing on the cake.

(8/15) x.com

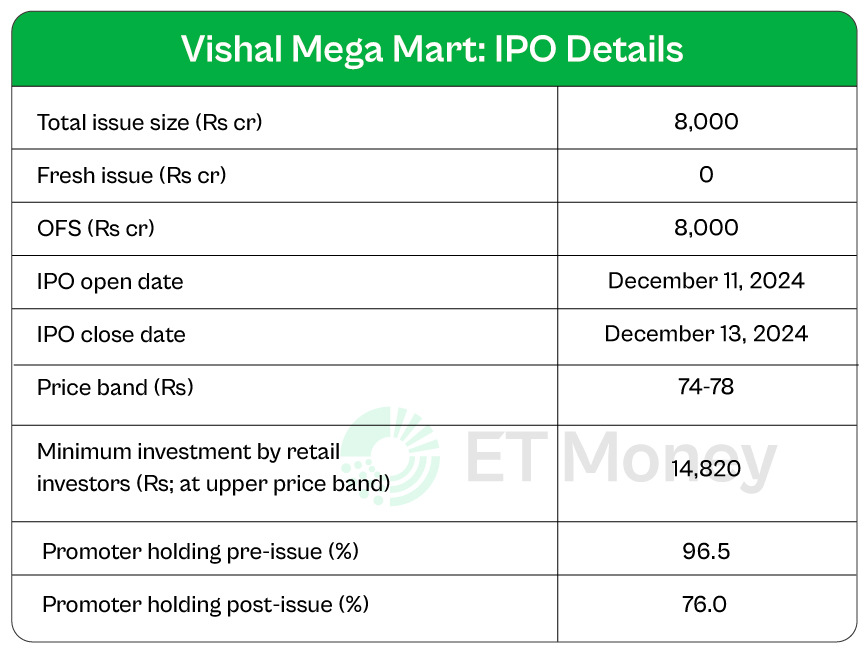

4. Key IPO details

Vishal Mega Mart's IPO is entirely OFS (Offer for sale).

This means the money raised through the IPO will not be used for the company’s business expansion.

The IPO proceeds will go to the promoters. This isn’t a good sign.

Here are other key details. 👇

(9/15)

Vishal Mega Mart's IPO is entirely OFS (Offer for sale).

This means the money raised through the IPO will not be used for the company’s business expansion.

The IPO proceeds will go to the promoters. This isn’t a good sign.

Here are other key details. 👇

(9/15)

Before we wrap up, let's review the company's key risks.

- It relies on external vendors for their branded products (no in-house production)

- 35% of its stores (226 out of 645) are concentrated in Uttar Pradesh, Karnataka, and Assam

(10/15)

- It relies on external vendors for their branded products (no in-house production)

- 35% of its stores (226 out of 645) are concentrated in Uttar Pradesh, Karnataka, and Assam

(10/15)

5. Strengths & Concerns

Let’s first look at the positives.

It’s a trusted brand with strong consumer recall.

With 70% of revenue from in-house brands, it has better control over margins.

The company boasts solid financials, and its valuations are not steep.

(11/15)

Let’s first look at the positives.

It’s a trusted brand with strong consumer recall.

With 70% of revenue from in-house brands, it has better control over margins.

The company boasts solid financials, and its valuations are not steep.

(11/15)

Now, let’s review some of the key concerns.

The entire IPO is OFS.

Heavily relies on vendors for manufacturing.

High competition plus limited differentiation could pose challenges.

(12/15)

The entire IPO is OFS.

Heavily relies on vendors for manufacturing.

High competition plus limited differentiation could pose challenges.

(12/15)

WRAP UP

IPO promises strong growth, solid margins, and appealing valuations.

That said, regional dependency, vendor reliance, and an OFS-only issue are key risks.

If you're after growth at a fair price, Vishal has potential—but weigh the risks carefully.

(13/15)

IPO promises strong growth, solid margins, and appealing valuations.

That said, regional dependency, vendor reliance, and an OFS-only issue are key risks.

If you're after growth at a fair price, Vishal has potential—but weigh the risks carefully.

(13/15)

(14/15)

Will you invest in this IPO?

Will you invest in this IPO?

(15/15)

If you found this useful, show some love.❤️

Please like, share, and retweet the first tweet. 👇

x.com

If you found this useful, show some love.❤️

Please like, share, and retweet the first tweet. 👇

x.com

Correction: There’s a typo in the image attached to the 5th tweet. The last column in the table does not represent FY23 numbers as mentioned. Instead, it shows figures for FY22.

Correction: There’s a typo in the image attached to the 5th tweet. The last column in the table does not represent FY23 numbers as mentioned. Instead, it shows figures for FY22.

Loading suggestions...