$32 billion.

That is how much Uber is estimated to have lost building their business.

Everyone knows ride-hail is a network effects business.

And Uber was dominant.

So why weren't they profitable much earlier?

🧵 x.com

That is how much Uber is estimated to have lost building their business.

Everyone knows ride-hail is a network effects business.

And Uber was dominant.

So why weren't they profitable much earlier?

🧵 x.com

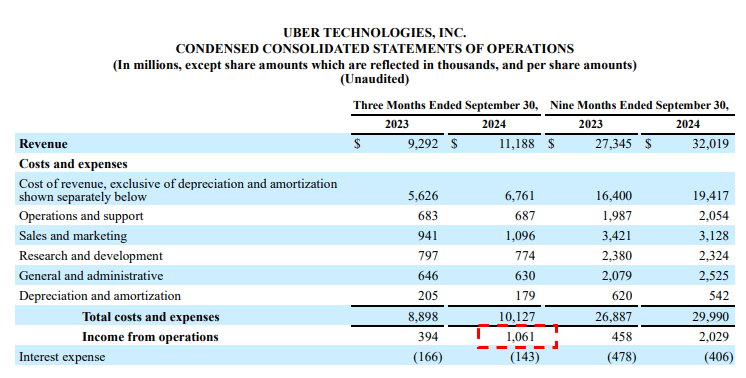

$Uber was the poster child of money-losing VC-backed start-up.

Many thought they would never acheive profitability.

However, last quarter alone they generated $1bn in GAAP operating profit (!)

What changed?

(2/15) x.com

Many thought they would never acheive profitability.

However, last quarter alone they generated $1bn in GAAP operating profit (!)

What changed?

(2/15) x.com

Most investors would think a dominant player in a internet-enabled business that benefits from local network effects would easily achive profits,

but that wasn't the case.

One pesky competitor, $LYFT, kept them in the red for years.

(3/15) x.com

but that wasn't the case.

One pesky competitor, $LYFT, kept them in the red for years.

(3/15) x.com

Customer acqustion costs weren't exactly the problem.

It was retention costs.

A typical LTV/CAC model shows the value of a user compared to the cost to acquire them.

Their models didn't assume that they would...

(4/15) x.com

It was retention costs.

A typical LTV/CAC model shows the value of a user compared to the cost to acquire them.

Their models didn't assume that they would...

(4/15) x.com

have to keep *reacquiring* the same user after a competitor stole them.

This happened because the subsidies needed to steal a user (say $20) were less than the hypothesized LTV (say $200).

So they kept giving away $20 to get $200,

but they made a big mistake...

(5/15) x.com

This happened because the subsidies needed to steal a user (say $20) were less than the hypothesized LTV (say $200).

So they kept giving away $20 to get $200,

but they made a big mistake...

(5/15) x.com

With all of the aggresive rider subsidies,

no riders were staying for the full "lifetime"

They would switch apps as soon as they got a promo

While the ride-hail economics at *maturity* made sense...

(6/15) x.com

no riders were staying for the full "lifetime"

They would switch apps as soon as they got a promo

While the ride-hail economics at *maturity* made sense...

(6/15) x.com

... competition funded by VC's meant that they would never get there.

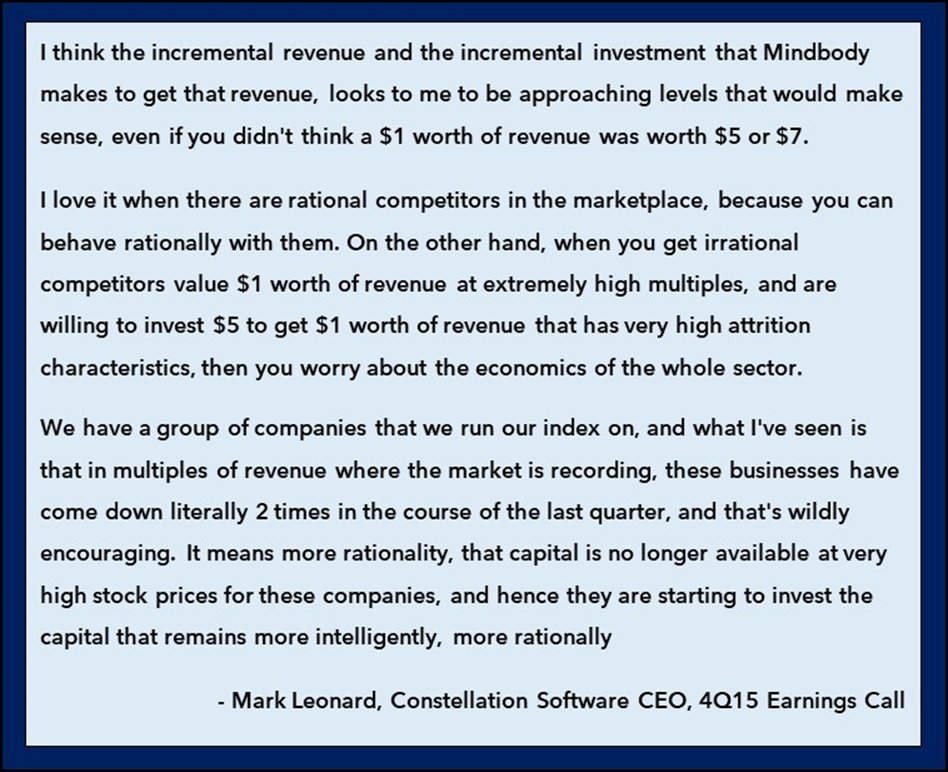

Below is Mark Leonard commenting on this dynamic in SaaS in 2015.

A high revenue multiple of 7x meant a company could spend $5 for a $1 of revenue and still create $2 of market cap.

BUT...

(7/15) x.com

Below is Mark Leonard commenting on this dynamic in SaaS in 2015.

A high revenue multiple of 7x meant a company could spend $5 for a $1 of revenue and still create $2 of market cap.

BUT...

(7/15) x.com

...when valuations fell to a normal level,

they would be forced to spend more rationally.

So what changed in the Uber vs Lyft industry dynamics?

(8/15) x.com

they would be forced to spend more rationally.

So what changed in the Uber vs Lyft industry dynamics?

(8/15) x.com

Lower Driver CAC

1) Lyft lost their drivers during Covid and had to work hard to bring them back.

Uber Cross-seeded drivers to food delivery and vice versa (especially during Covid) which meant better driver retention--and recovery after Covid.

(9/15)

1) Lyft lost their drivers during Covid and had to work hard to bring them back.

Uber Cross-seeded drivers to food delivery and vice versa (especially during Covid) which meant better driver retention--and recovery after Covid.

(9/15)

2) As Lyft struggled to rebuild their driver network, users saw quicker times and lower prices on Uber.

Classic network effects explains that more users meant more business for Uber drivers, further pushing drivers to ditch Lyft.

(10/15) x.com

Classic network effects explains that more users meant more business for Uber drivers, further pushing drivers to ditch Lyft.

(10/15) x.com

Valuations Fall

3) Lower valuations meant money-losing subsidies couldn't be funded,

and it no longer made economic sense to fight for share.

Investor's started pushing for profits.

(11/15)

3) Lower valuations meant money-losing subsidies couldn't be funded,

and it no longer made economic sense to fight for share.

Investor's started pushing for profits.

(11/15)

Better User Retention

4) Less aggresive competitor subsidies meant less of a reason to churn.

5) Uber's lower wait times and better prices meant less user defections

6) The Uber One Loyalty program reduced fees for users, provided they commit to one provider

(12/15)

4) Less aggresive competitor subsidies meant less of a reason to churn.

5) Uber's lower wait times and better prices meant less user defections

6) The Uber One Loyalty program reduced fees for users, provided they commit to one provider

(12/15)

New Products

6) Adding advertising to the app created a new revenue stream at no additional cost

(13/15)

6) Adding advertising to the app created a new revenue stream at no additional cost

(13/15)

Thus after burning billions in capital, industry dynamics finally rationalized in 2023.

Uber made their first GAAP profit.

And the theoretical "steady-state" economics started to be proven out.

(14/15) x.com

Uber made their first GAAP profit.

And the theoretical "steady-state" economics started to be proven out.

(14/15) x.com

This is just the narrative we see though.

If you think we forgot some factors, please comment below!

And if you liked this thread, help share it by liking the below tweet! 🙏

(15/15)

x.com

If you think we forgot some factors, please comment below!

And if you liked this thread, help share it by liking the below tweet! 🙏

(15/15)

x.com

Loading suggestions...