In this story, we’ll dive into what’s being called the worst housing affordability crisis in over a decade. From London to Mumbai, housing markets are at a critical juncture.

Let’s break down what’s happening globally and here at home in India.

Let’s break down what’s happening globally and here at home in India.

Housing is a topic worth discussing because the International Monetary Fund (IMF) recently published a series of perspectives on housing markets around the world in its Finance and Development magazine.

These insights were fascinating, so we’ve summarized them for you.

These insights were fascinating, so we’ve summarized them for you.

First, the big picture: Housing isn’t just about having a roof over your head. For most people, it’s the biggest source of both wealth and debt.

It’s central to economic stability and represents security and a sense of belonging. But right now, that dream is slipping away for many, especially young people.

It’s central to economic stability and represents security and a sense of belonging. But right now, that dream is slipping away for many, especially young people.

The numbers are alarming.

According to new research from the IMF, housing is less affordable today than it was during the bubble that led to the 2008 financial crisis.

The crunch is hitting hardest in countries like the United States, United Kingdom, Australia, Canada, Germany, Portugal, and Switzerland.

In the U.S., housing affordability has dropped from around 150 on the affordability index in 2021 to the mid-80s by 2024. The UK has seen a similar decline, from 105 to the low 70s. While the IMF’s research doesn’t cover India extensively, we’ll get to the local situation shortly.

According to new research from the IMF, housing is less affordable today than it was during the bubble that led to the 2008 financial crisis.

The crunch is hitting hardest in countries like the United States, United Kingdom, Australia, Canada, Germany, Portugal, and Switzerland.

In the U.S., housing affordability has dropped from around 150 on the affordability index in 2021 to the mid-80s by 2024. The UK has seen a similar decline, from 105 to the low 70s. While the IMF’s research doesn’t cover India extensively, we’ll get to the local situation shortly.

One fascinating aspect of this crisis is the psychological element driving it. It’s not just about interest rates—those account for only about a quarter of the changes in affordability over the past fifty years.

What’s really pushing prices up is human behavior: the fear of missing out, combined with social beliefs that housing prices always go up.

This creates a powerful cycle that keeps pushing the market higher.

What’s really pushing prices up is human behavior: the fear of missing out, combined with social beliefs that housing prices always go up.

This creates a powerful cycle that keeps pushing the market higher.

There’s also a generational divide. While older generations benefited from rising housing prices since the 1980s, building wealth through home equity, today’s young people are facing a different reality.

Many can’t even afford to rent, let alone buy a home.

Many can’t even afford to rent, let alone buy a home.

So, what’s driving this crisis?

It’s a perfect storm. High interest rates are pushing up mortgage costs, but the bigger issue is supply. Housing is severely constrained by zoning laws and land-use restrictions. Take Canada, for example.

The country needs around 500,000 new homes each year to meet demand, but over the past two decades, they’ve been building just 150,000 to 250,000 annually.

It’s a perfect storm. High interest rates are pushing up mortgage costs, but the bigger issue is supply. Housing is severely constrained by zoning laws and land-use restrictions. Take Canada, for example.

The country needs around 500,000 new homes each year to meet demand, but over the past two decades, they’ve been building just 150,000 to 250,000 annually.

Another surprising element is how house prices behaved during the COVID-19 recession.

Unlike previous downturns where housing markets weakened, prices actually surged. Even as central banks raised interest rates to fight inflation, housing prices haven’t fallen as much as experts expected.

There’s also a darker side to the story.

Unlike previous downturns where housing markets weakened, prices actually surged. Even as central banks raised interest rates to fight inflation, housing prices haven’t fallen as much as experts expected.

There’s also a darker side to the story.

Criminal networks and corrupt politicians are using luxury real estate to hide illicit wealth, particularly in cities like New York, Miami, London, and Dubai.

In London alone, foreign companies held £73 billion worth of properties in 2018, with 90% of these purchases made through tax havens.

In London alone, foreign companies held £73 billion worth of properties in 2018, with 90% of these purchases made through tax havens.

This has sparked a global backlash against foreign buyers.

Australia has tripled fees for foreigners buying existing houses. New Zealand banned foreign buyers from purchasing certain residential properties in 2018, and Canada has extended its foreign buyer ban to 2027.

Even Singapore, which has traditionally welcomed foreign investment, doubled its stamp duty for foreign buyers to 60%.

Australia has tripled fees for foreigners buying existing houses. New Zealand banned foreign buyers from purchasing certain residential properties in 2018, and Canada has extended its foreign buyer ban to 2027.

Even Singapore, which has traditionally welcomed foreign investment, doubled its stamp duty for foreign buyers to 60%.

Now, let’s look at India.

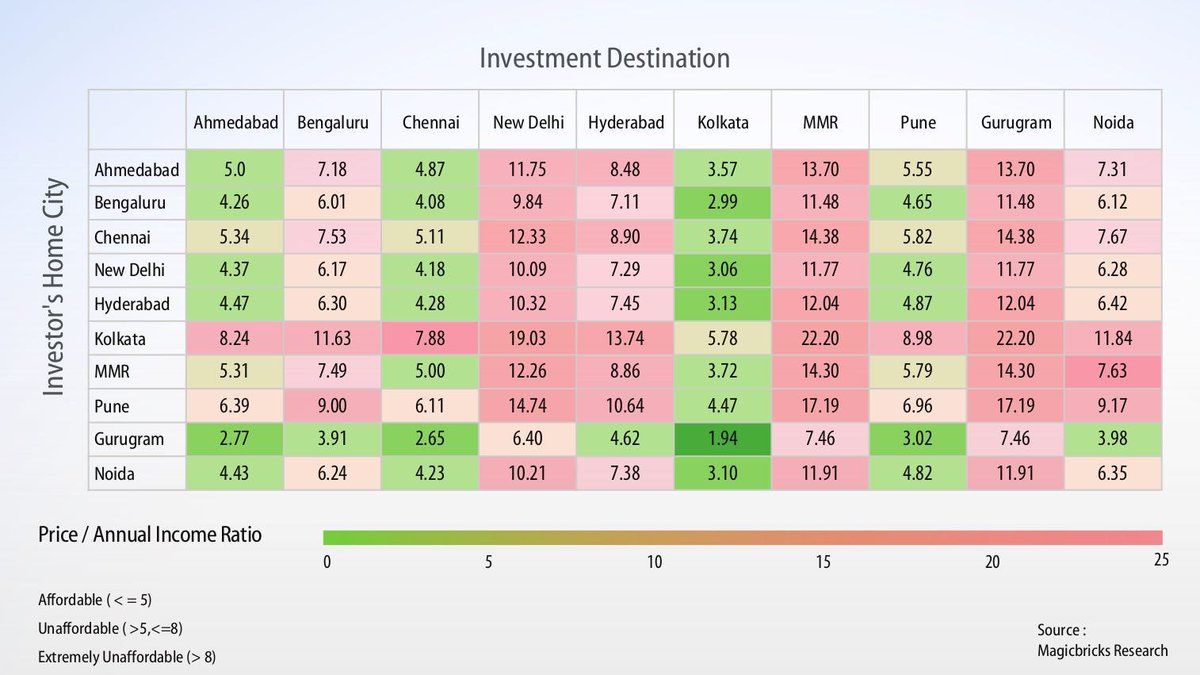

A report by real estate portal Magicbricks shows that the price-to-income ratio in India has hit 7.5, much higher than the globally accepted level of 5.

The price-to-income ratio essentially tells you how many years of your annual income it would take to buy a house. Ideally, this number should be 5 or below.

A report by real estate portal Magicbricks shows that the price-to-income ratio in India has hit 7.5, much higher than the globally accepted level of 5.

The price-to-income ratio essentially tells you how many years of your annual income it would take to buy a house. Ideally, this number should be 5 or below.

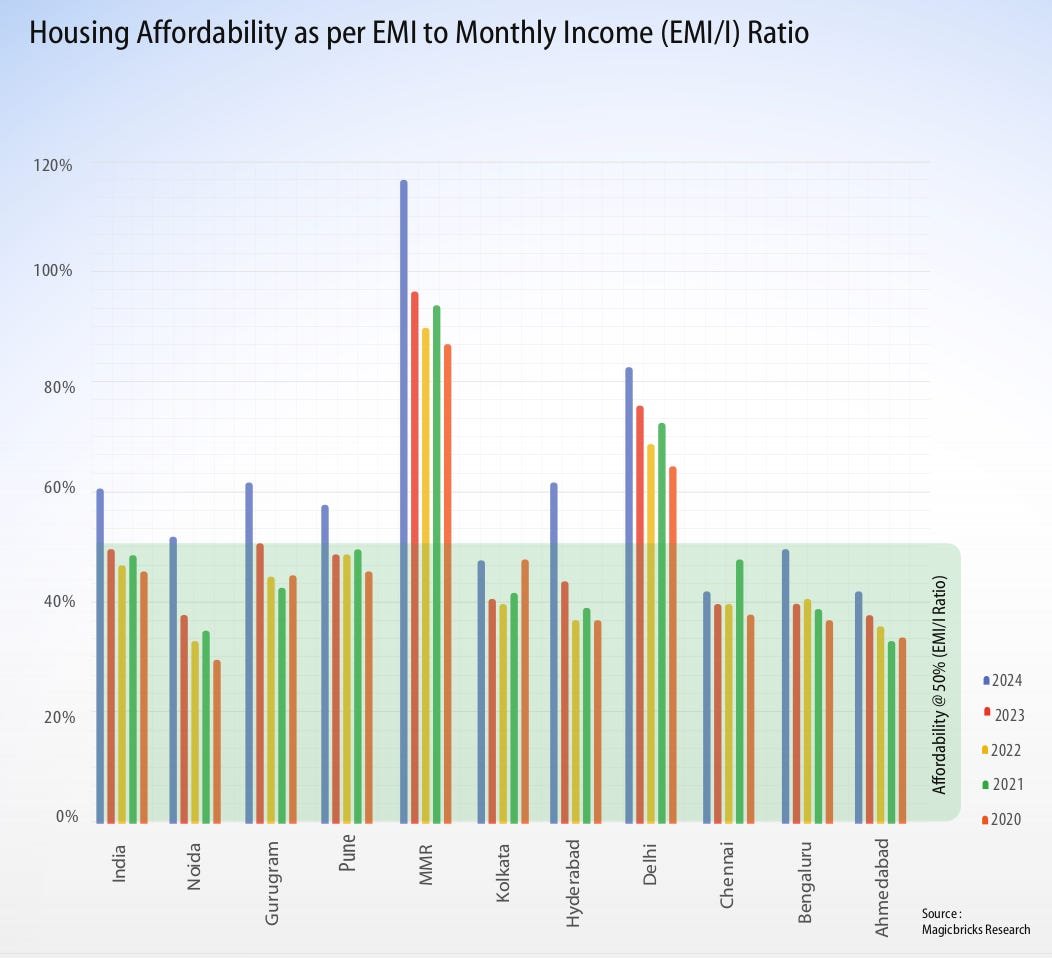

It’s concerning that Indians are now spending around 61% of their income on housing costs. That’s far above the 50% mark considered sustainable.

The impact of this varies a lot depending on the city. In places like Chennai, Ahmedabad, and Kolkata, housing remains relatively affordable, with people spending 41-47% of their income on it.

But in the Mumbai Metropolitan Region, the number skyrockets to an unbelievable 116%. Delhi isn’t much better at 82%.

The impact of this varies a lot depending on the city. In places like Chennai, Ahmedabad, and Kolkata, housing remains relatively affordable, with people spending 41-47% of their income on it.

But in the Mumbai Metropolitan Region, the number skyrockets to an unbelievable 116%. Delhi isn’t much better at 82%.

There might be some relief on the horizon. A report from Magicbricks suggests that as more housing supply comes into the market, price growth could slow down.

Stronger economic fundamentals and better global growth prospects might also lead to a slight drop in interest rates.

Stronger economic fundamentals and better global growth prospects might also lead to a slight drop in interest rates.

Still, the solution isn’t just about waiting for prices to go down. Experts believe we need to address deeper issues.

That means cutting through regulatory hurdles, providing targeted support to low-income families, and rethinking zoning laws that limit housing supply.

As Alan Kohler aptly put it, “It’s a global housing affordability crisis, but each country is unhappy in its own way.”

That means cutting through regulatory hurdles, providing targeted support to low-income families, and rethinking zoning laws that limit housing supply.

As Alan Kohler aptly put it, “It’s a global housing affordability crisis, but each country is unhappy in its own way.”

We cover this and one more interesting story in today's episode of the Daily Brief. You can watch the episode on YouTube, read on Substack, or listen on Spotify, Apple Podcasts, or wherever you get your podcasts. All links here:

thedailybrief.zerodha.com

thedailybrief.zerodha.com

Loading suggestions...