Re: Inflation/USD Wrecking Ball-Who's Gonna Out-Hawk the Fed?

When I think about the relative capacities for CB's to embrace "Higher For Longer" policies, I still don't think anyone can out-hawk the Fed. (MINI-THREAD)

When I think about the relative capacities for CB's to embrace "Higher For Longer" policies, I still don't think anyone can out-hawk the Fed. (MINI-THREAD)

I've been expressing this sentiment for a while. CB's can jawbone, but they have yet to back up tough talk with tough action.

There are many reasons why I think RoW's CB's will be hard-pressed to narrow interest rate differentials between the US and their respective regions. The first reason is just relative economic strength.

The Eurozone's economy has proven far more resilient in the face of the Russia/Ukraine war than many expected, and that likely has emboldened La Garde's recent hawkish jawboning. BUT I think Mother Nature may have given Europe a pass -- for now.

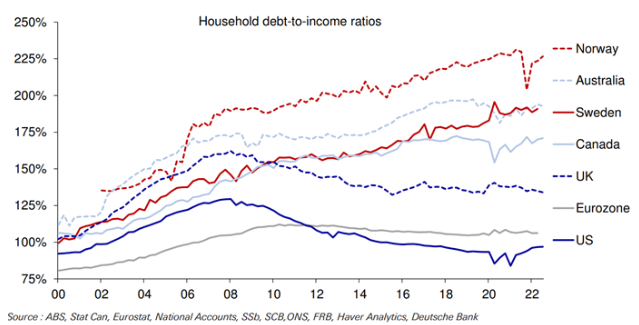

There are other reasons for why the US economy is likely to be more resilient than RoW -- the US has one of the lowest household debt-to-income ratios in the world. H/t DB.

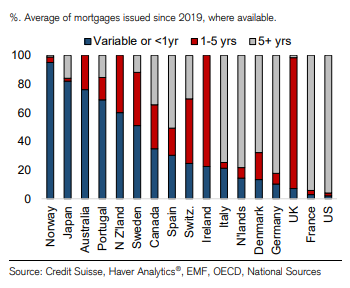

Related to this theme, the US also has one of the lowest percentages of variable-rate mortgages in the world. This is a key reason why the CB's of Canada and Australia both stepped down earlier than the Fed. H/t CS and @PauloMacro for flagging this chart.

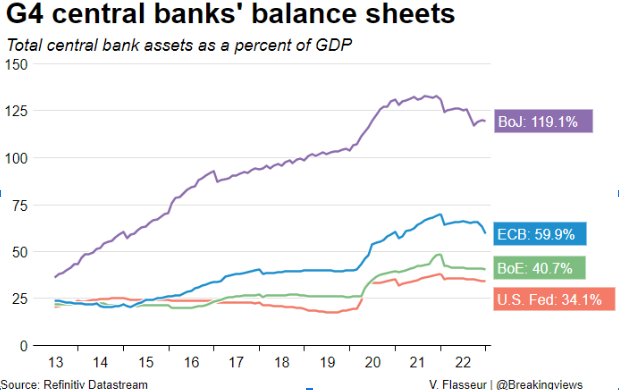

But it doesn't end with relative economic strength. There's also the little issue of CB balance sheets. H/t Refinitiv.

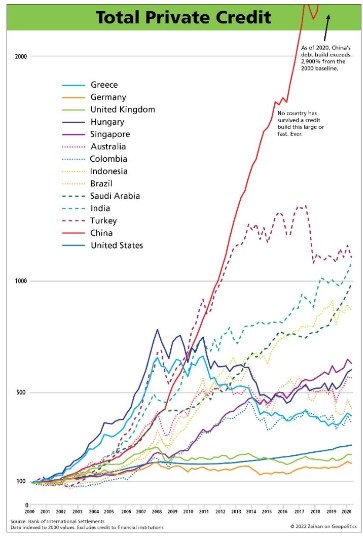

What about China? Given the obfuscatory interplay between the PBOC and state banks in China, it's harder to find a clean apples-to-apples analog, but many believe China is in the worst shape of all when it comes to the debt straitjacket. H/t @PeterZeihan

The conflicting incentives between CB's and the Fed are stark and yet issues like Japan's YCC and BOE's Gilt problem have largely been swept under the rug by this breather in the USD Wrecking Ball. I talked about these issues at length here:

For all of these reasons, I think 2023 may herald a resurgence in the USD Wrecking Ball. Technically, I think there could be another flush to wring out some last spec longs, but I think we might be close to a ST bottom.

I'm going to end with a geopolitical angle to all this -- I think the relative capacity for the Fed to go "Higher For Longer" gives the US the ability to wield the USD Wrecking Ball as a Geopolitical Lever in the name of fighting inflation.

I have been busy working on a position paper about this topic to present at West Point next month. I look forward to previewing some of these thoughts with @MikeIppolito_ tomorrow on his podcast. (END THREAD)

Getting close here. I wanna see JPY breach 127, GBP breach 1.24, and EUR breach 1.09.

Just a reminder that “USD is dead” predictions have been around a LONG time. Half these books are from the 1970’s.

@SantiagoAuFund

@SantiagoAuFund

LGFV = Let Go of Fucking Value

zerohedge.com

zerohedge.com

The US has belatedly taken action in the Semiconductor Industry, matching proactive industrial policy with punitive economic coercion. There are lessons here that need to be extrapolated to the Oil & Gas Industry, and that is something our paper addresses.

See the chart above? Then look below. Now look me in the eye and tell me that the BOJ is gonna sacrifice JGB’s in the name of saving the JPY.

Lots of comments about the Nixon Shock of 1971 and the “untethering” of USD from Gold. My counter: what then prompted the rise of Eurodollar banking in the 1950’s? Why did the market organically choose to use USD over and above its Gold backing then?

👆This is a topic @MikeIppolito_ and I chatted at length about today and is a key focus of my West Point collaboration.

Honestly not sure of the denouement here. BOJ is facing a lose/lose here, and that is why I don't buy the arguments that we will resort to YCC here.

This is pretty incredible.

BOJ's moment of reckoning is here. Will it 1) rescue JGB's, 2) defend JPY, or 3) institute capital controls? It's clearly trying the #1 first, but JPY ain't buying it.

That 25 bp relaxing of the YCC band is getting costlier by the minute.

BOJ be like William Wallace.

The continued implosion of TTF / NBP is the fly in the ointment for my thesis that "ECB/BOE can't out-hawk the Fed." Imho, nice weather tends to gird CB loins -- at least across the Atlantic.

Getting pretty crowded.

I've officially broken my trading hiatus since before Christmas and have gone long the USD Wrecking Ball as my first trade of 2023.

Heh. She can talk the talk, but doesn't wanna walk the walk.

When I juxtapose this to the chart above, what country is the most fucked in terms of "Scylla vs. Charybdis" choices? 🤔

TLDR version of this thread:

This is very much a topic I am exploring.👇

BOJ hath spoken and JPY (left) and JGB yields (right) are listening.

The podcast with @MikeIppolito_ is up.👇

Markets to ECB: “You can talk the talk; now walk the walk. Zzzz.”

The US economy appears very fit still. Or should I say “fitty,” which in my town connotes 50?

Loading suggestions...